A group of conservative Republicans representatives known as the House Freedom Caucus came out last week against any proposal that would lift the cap on deposit insurance, currently set at $250,000. Members of US Congress on both sides of the aisle are understandably cautious about taking such a dramatic step in the middle of an unfolding crisis.

The dollar has lost some of its luster over the winter. The twin supports of its status as the preferred haven during the pandemic and being backed by the world’s strongest economy are fading.

Congress is asking the Federal Reserve and other financial regulators what went wrong at Silicon Valley Bank and why they didn’t see it coming. In due course, they’ll admit some mistakes, draw some lessons and tweak some rules.

I’ve received more emails and calls from clients on the failure of SVB Bank than I did on the stock market crash in April of 2020. That tells me there is wide concern today about the stability of the economy and financial markets.

Here is what sets rockstars apart from the average advisor.

There are many marketing initiatives you can implement on your own that that will likely work. Here are some suggestions.

The goal of marketing is to garner loyalty among existing clients while also attracting new ones to drive growth and profitability for your firm. To implement engaging messaging, follow these tips…

Here are the core tenets I share with advisors who are trying to carve their niche and stand out – the best practices to beef up your marketing efforts in 2023.

Here are six compliance-friendly ways to incorporate social proof into your website to establish trust and capture new leads.

A study, reported in the Harvard Business Review, claimed that likability was not important to the sales process.

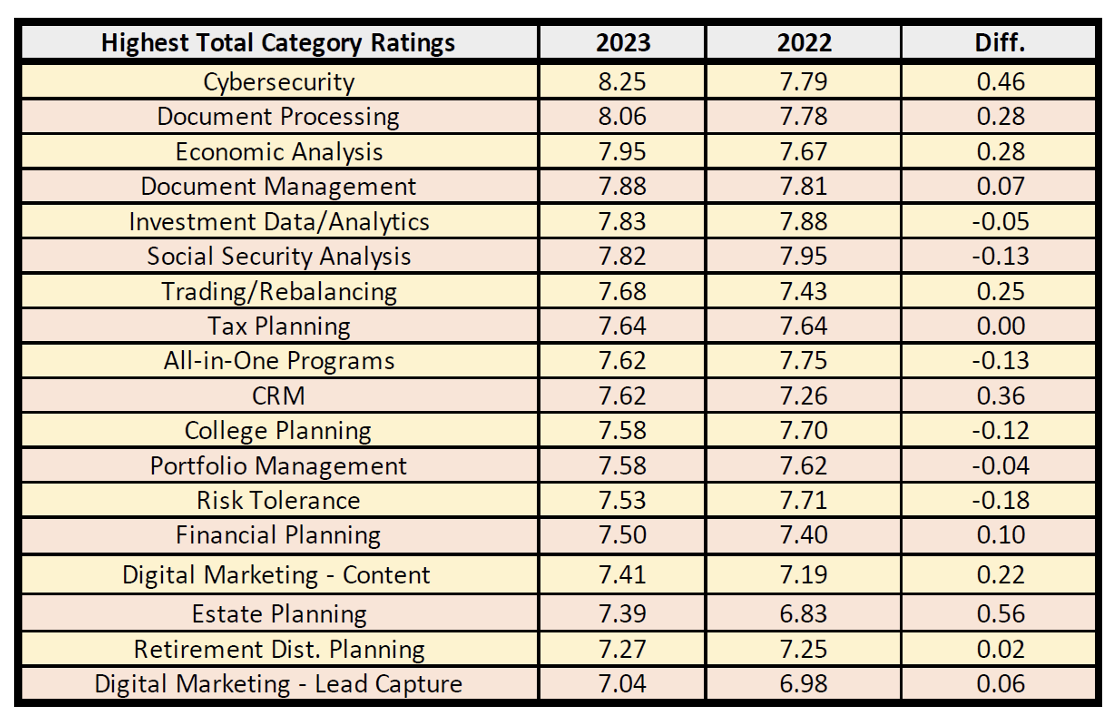

The 2023 T3/Inside Information Software Survey is now available. It’s the best guide to the 300+ fintech solutions in the marketplace, and a good buyer’s guide for advisory firms that are looking for additions or enhancements to their tech stack.

In hindsight, it was obvious it wouldn’t last. Low interest rates — the result of shifts in the global economy, economic stability, low inflation and monetary policy — couldn’t stay at zero forever.

A year into its fight against inflation, the Federal Reserve could — just maybe — be done raising its policy rate. History shows that monetary policy pauses mark great buying opportunities for US stocks, but there are several key caveats to bear in mind this time.

For millions of borrowers, student loan forgiveness will mean the difference between significant relief and ongoing payments. If you’re among them, the question is… what next?

The sudden loss of confidence by depositors in some US banks is causing many to focus on the scope for financial contagion and the needed policy responses. What should not be overlooked is the other, and slower, contagion channel in play — that involving enablers of economic growth...

With all that extra intelligence, there will be a need and a desire to undertake many new projects, ranging from innovative theatrical productions to more efficient and densely packed solar panels. These new projects could also herald a world of much cheaper and greener energy, which would further increase humankind’s ability to manipulate the natural environment. Land will thus become more valuable.

The changes inside SECURE 2.0 range from new rules related to 529 college savings plans to when retirees should take their required minimum distributions (RMDs). With so much to sort through, advisors may be overlooking some of the details of the act.

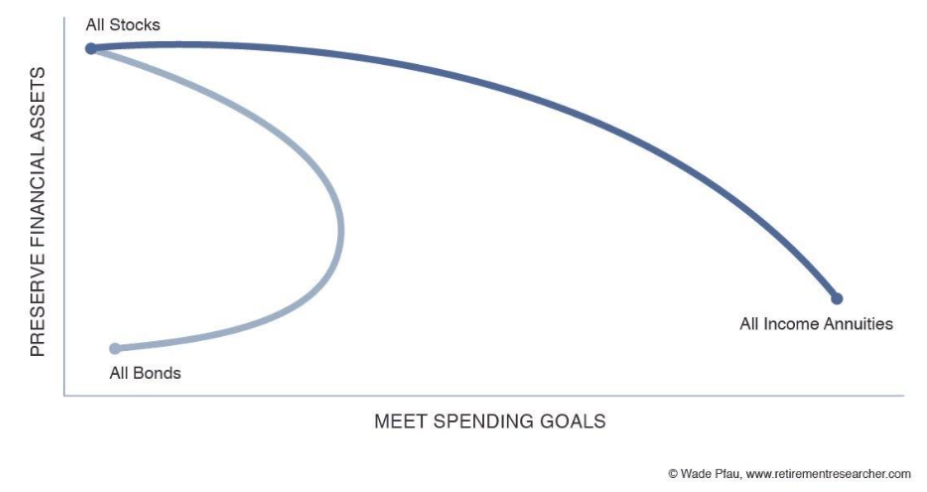

A simple annuity can effectively replace bond holdings in a retirement plan that are earmarked to meet the lifetime spending goal. The question is why should a retiree hold any bonds in the portion of their asset base designed to cover ongoing retirement spending goals?

The economic signals and a host of geopolitical risks confronting investors suggest that 2023 could be as challenging as 20022 for both stocks and bonds.

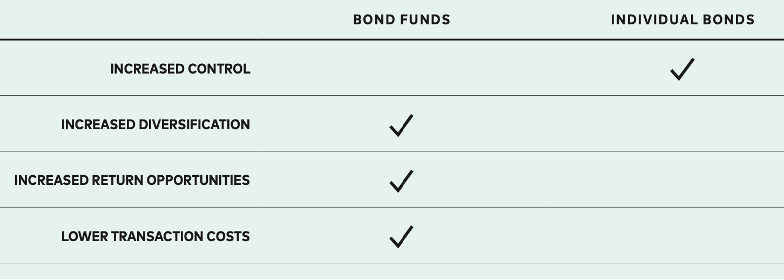

Should investors build their own portfolios of bonds, or buy shares of bond funds? Is there an economic difference or just one of appearance? Are directly held bonds safer because they mature, and you get your money back? How should one decide?

Annie Duke, once one of the best female poker players in the world, helped me understand why people work longer than they need to. This got me thinking about the decumulation problem more broadly and planning to live to age 100.

Of all the questions that ChatGPT has raised about the future of artificial intelligence, one still reverberates through Silicon Valley: Why couldn’t the industry’s largest technology firms breed an innovative service with a similar kind of impact, especially after amassing some of the world’s largest AI teams?

For all of you following the banking crises in the US and Europe, and asking why this is all happening again, I have bad news: Regardless of what laws are passed, or which regulations are issued, banking crises will recur — and not infrequently.

The pitch for an actively managed bond exchange-traded fund can be compelling, especially when there’s market turmoil and uncertainty

It’s rarely mentioned, but it’s stunning how often the financial planning profession has foreshadowed the evolution of our social environment.

Advisors have always considered the discovery meeting unchallengeable. Why?

In this interview, noted economist Woody Brock discusses what exactly causes gridlock, and how can its grip be broken.

The importance of Biden’s veto to save the DOL rule was not about assessing ESG factors. It was about affirming the role of the fiduciary in investment advice.

Lower interest rates and more liquidity are the keys to boosting confidence in the financial sector, but they impede the Fed's ability to fight inflation.

The Federal Reserve raised interest rates by a quarter percentage point and signaled it’s not finished hiking, despite the risk of exacerbating a bank crisis that’s roiled global markets.

I’ll explore four tools and strategies you can leverage to improve how your site ranks in search engines to reach your clients and prospects more effectively.

I am drained having my colleagues and team members come to me with problems because of their frustration with my company.

There are five reasons why prospects decide to choose someone else.

Do advisors need to accept that technology will forever be a drag, or can the right approach lead to personal happiness and a more productive practice?

All eyes in the financial and economic world will be laser-focused Wednesday on the Federal Reserve as Chair Jerome Powell tries to balance his fight against inflation against a sudden banking crisis.

Easing financial conditions globally have made Morgan Stanley “outright bullish” on growth stocks in Asia and emerging markets versus their value peers.

A Singapore-based fintech investment firm is close to raising $100 million to back finance and blockchain startups in China and Southeast Asia.

A question has arisen amid all the bank failures. How, with the bond market enduring its worst spasm of volatility in almost four decades, have benchmark-level stocks managed to glide along, oases of calm?

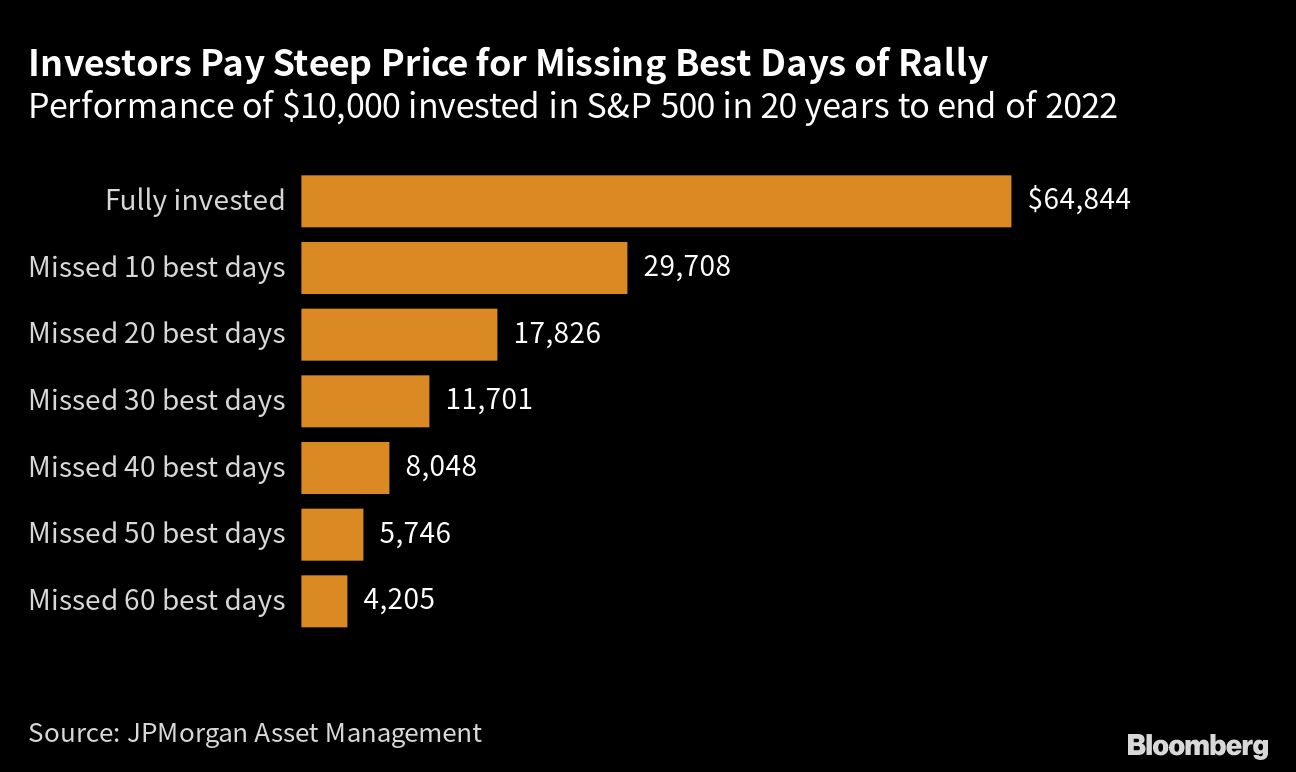

Some of the world’s biggest investors are looking beyond interest-rate hikes, bank failures and the threat of recession to one of the greatest fears of all money managers — missing out on the next big rally.

US officials are studying ways they might temporarily expand Federal Deposit Insurance Corp. coverage to all deposits, a move sought by a coalition of banks arguing that it’s needed to head off a potential financial crisis.

When I hear of advisors spending $80,000 on marketing and getting zero clients, as one advisor shared with me recently, I envision a revolving door.

You provide a lot of value to your clients. Save them from making even a single catastrophic financial mistake and your fees will forever be a moot point.

If you work with boomer-generation women, are you properly responding to their need for lifetime income? Consider this parable.

The best way to preemptively avoid paying unnecessary fees is by checking before the services are consumed.

Steve Chiavarone doesn’t want to scare anyone, but what he remembers most from the last banking crisis was how sure most people were that it wouldn’t happen.

Markets have been trading as if the end of the world is at hand – but what most participants see, behind the recent financial turmoil and contagion fears, is a still-strong US economy, the MLIV Pulse survey shows.

UBS Group AG agreed to buy Credit Suisse Group AG in a historic, government-brokered deal aimed at containing a crisis of confidence that had started to spread across global financial markets.

The strongest force standing in the way of nuclear energy is the antiquated, irrational fear of it.

New research confirms the valuable role that short sellers play in correcting the valuations of overpriced stocks.

A TIPS is risky in the short term and riskless in the long run, which is precisely the opposite of, and complementary to, a T-bill, which is riskless in the short term but, because of reinvestment rate volatility, risky in the long run.