Read Michael Contopoulos' latest report highlighting opportunities outside of Investment Grade corporate bonds and why one does not need to own credit to generate income at the moment.

Stocks lower as investors digest data, Fed commentary.

With the new year in its infancy, it may be too early to think about where to spend Thanksgiving or booking your car’s fall tune-up.

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

US workers are clearly feeling the strain of economic uncertainty, according to Franklin Templeton’s third annual “Voice of the American Worker” study.

Differing economic cycles and limited trade links will make the sur unfeasible.

Brian Smedley, Chief Economist and Head of the Macroeconomic and Investment Research Group, joins Macro Markets to discuss Fed policy, recent inflation, labor, and GDP data, and key takeaways for investors from our 10 Macroeconomic Themes for 2023.

Inflation has turned a corner, but not yet for food.

Investors should be aware of potential real-time market exposure risks when implementing large changes to their portfolios.

Monday’s trading saw oil rise as traders digested China’s return in demand against a continued supply strain and slower growth in world economies.

Changes for investors include RMD age increases, higher catch-up contribution limits and a new 529 transferal option.

Valuation metrics across all but the U.S. interest rate dimension remain unambiguously attractive.

With Caixin China PMI numbers today broadly confirming Monday’s official CCP data, the outlook for China and its neighbors remains bright.

At the beginning of the season, not many predicted that the Philadelphia Eagles would be in the Super Bowl this year.

The European Central Bank raised its policy rate, and more hikes are coming.

The most recent NFIB (National Federation Of Independent Business) is sending a strong signal of an economic recession.

Markets are no longer shocked by central bank tightening.

We are now seeing clear signs of a broad-based decline in inflation.

These weekly letters, of which I’ve now written well over 1,000 (plus 7 books and multiple papers and articles), are generally about two broad topics: the economy and the financial markets. While related, these aren’t the same. Good news for one can be (and often is) bad news for the other.

Retail demand for bars and coins in the U.S. and Europe hit a new annual record last year in response to stubbornly high inflation and the war in Ukraine. Western investors gobbled up 427 tons (approximately 15 million ounces), the most since 2011.

Chief Economist Eugenio J. Alemán discusses current economic conditions.

The April Live Cattle futures, LCJ23, rallied as traders digested the United States Department of Agricultures (USDA) Cattle inventory report.

From a contrarian investing view, everyone remains bearish despite a market that corrected all of last year.

At the conclusion of its inaugural policy meeting of 2023 today, the U.S. Federal Reserve (Fed) delivered a smaller, quarter-point rate hike, as widely expected by markets.

In 1965 I was studying for a degree in Engineering.

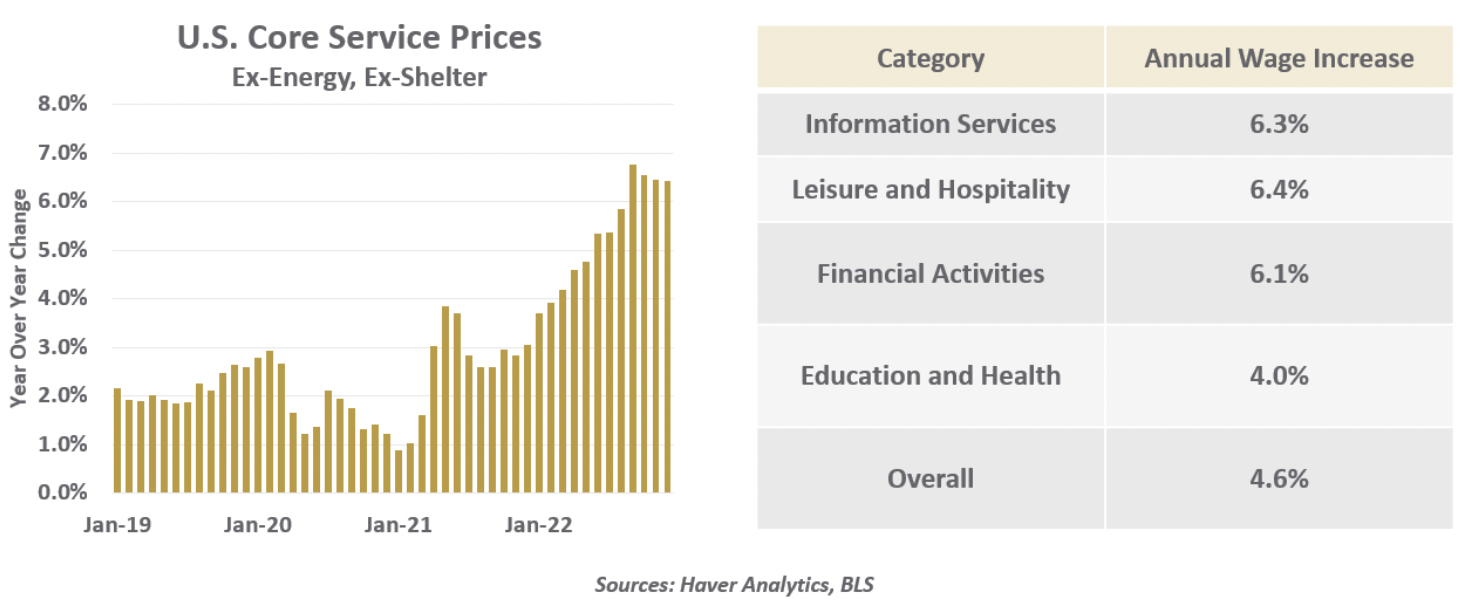

Inflation is a mixed picture, with services staying hot.

During uncertain economic times – as we are experiencing currently – the ever-important principles of valuation and margin of safety become even more important.

As expected and discussed in the January Macro Tides the December Consumer Price Index (CPI) dropped below 7.0% falling to 6.5% from 7.1% in November.

Investors face mixed signals between the Federal Reserve’s policy guidance and recent economic developments.

On Monday, Germany’s GDP print for the final quarter of 2022 came out below expectations of 0.0% by -2%.

US market structure was back in the news recently with several stocks experiencing irregular price movements on the morning of January 24.

The Fed downshifted to a smaller rate hike to start 2023, but the job is far from done.

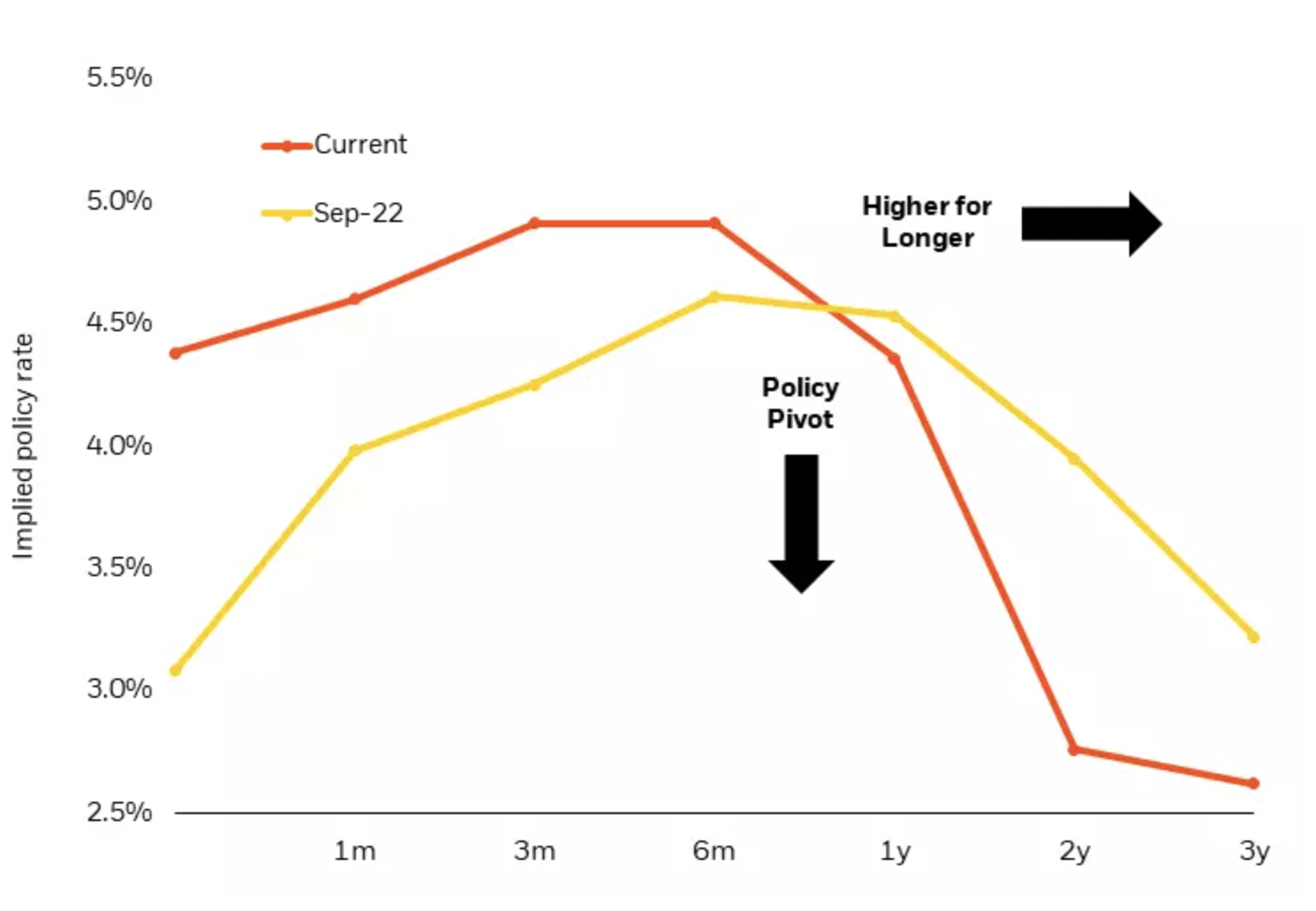

The market has high hopes for the Fed, however, comparing this to the Fed’s own expectations, we see a very different narrative.

Inflation appears to have peaked, led by improvements in core goods prices and rate-sensitive sectors like housing.

As investors seek to pinpoint market expectations for Federal Reserve policy, it’s critical to consider not just rate projections and derivatives pricing, but the degree of uncertainty and distribution of outcomes.

In anticipation of tomorrow’s rate decision, we saw another indicator today that the Federal Reserve has been successful in stemming the tide of inflation.

I chose the topic for this month’s Absolute Return Letter during the Christmas break.

It is hard to reconcile the jubilant mood of many business leaders with the uncertainty caused by the war in Ukraine.

A plunge in pricing power was one of the most notable developments we found in our latest quarterly survey of our credit analysts, who follow more than two dozen industries.

Review the latest Weekly Headings by CIO Larry Adam.

A slowdown in US economic activity this year is likely to impact most states, which could face budget deficits, according to Jennifer Johnston, Franklin Templeton Fixed Income’s Director of Municipal Bonds.

We are closing in on what we think may be the question of the decade. If a majority of stock market capitalization in the US is passive or indexed, does this cause problems for stock markets?

Guggenheim Investments’ Macroeconomic and Investment Research Group identifies 10 macroeconomic trends likely to shape monetary policy and investment performance this year.

2022 was a painful year in financial markets with almost all traditional assets delivering significant losses.

U.S. stocks declining, as the markets trim a strong start to 2023 ahead of this week's host of key economic and earnings data, as well as the Fed's monetary policy decision.

With wage growth still strong and unemployment low, the labour market is still historically tight. For now.

The US federal budget is on an unsustainable path…but not for the reasons that most people think.

Now is not the time to consider changing inflation targets.

Optimism is increasing on Wall Street, with investors hoping for a “soft landing” in the economy.

In stock investing there’s a management style called “growth at a reasonable price” or GARP. It seeks to achieve steadier results by avoiding both expensive growth stocks and beaten-down value stocks.