Capital represents the resources and labor used to produce goods and services.

As the second-largest economy in the world, China’s reopening has important economic and market implications. Here are some key considerations.

It appears to us at Smead Capital Management that investors are behaving in a way that will damage their capital and cause them to suffer stock market failure.

In 2023, the math of valuations suggests returns will likely be challenging as markets remain difficult to navigate.

What a difference a year makes!

The economics teams looks back at the most significant stories we covered during 2022.

The credit cycle and the economic cycle are excellent leading indicators of volatility.

Considering that a new year almost always brings surprises of one form or another, we've highlighted our top five that may define the global markets in 2023.

The Fed has massively inverted the yield curve. We explain why investors might be frontrunning themselves and why the long-term rate won’t budge.

Over the past two years, the US Federal Reserve has repeatedly erred in its analysis, policymaking, communications, and governance.

Structurally tight labor markets are providing support for tighter monetary policy, but the Fed may be fighting an uphill battle.

Inflation trends are moving in a favorable direction, but the change is likely too slow for the Fed to take its foot off the brake anytime soon.

This fall was a memorable time in the Halverson household.

As investors hope for a Santa Claus rally in the days ahead, the Grinch is looking to steal their holiday cheer.

This will be my last letter of 2022. I want to use this letter as a set-up for my annual forecast issue the first week of January. That means we will touch on a variety of topics, kind of a snapshot into where my mind is today. Get ready to travel the world but let’s start at home with the Federal Reserve meeting this week.

This important milestone is the culmination of decades’ worth of research and lots of trial and error, and it makes good on the hope that humanity will one day enjoy 100% clean and plentiful energy.

Chief Economist Eugenio J. Alemán discusses current economic conditions.

Stephen Dover, Head of Franklin Templeton Institute, shares his scorecard on some market prognostications for 2022, and what his team is watching in 2023—from blockchain to balanced portfolios.

The key takeaway from Wednesday’s FOMC meeting: despite encouraging inflation news, the Fed believes they have a long inflation fight ahead.

Will a dollar decline be good for stocks? It is an interesting question, given that during 2022 there was a significant non-correlation between the dollar and the stock market.

Scott Minerd, Global CIO for Guggenheim Partners and Chairman of Guggenheim Investments, joins the year-end episode of Macro Markets on Fed Day for a wide-ranging discussion of the Federal Reserve’s execution of monetary policy, economic conditions, the investment landscape for risk assets, portfolio strategy, and more.

The European Central Bank is likely to continue hiking rates next year, but the end point remains uncertain.

The Federal Reserve raised interest rates by a half point (50 basis points) on Wednesday in line with forecasts.

In part 1 I covered a model portfolio that was built on August 24, 2021, with the primary objective of generating a higher level of current income safely.

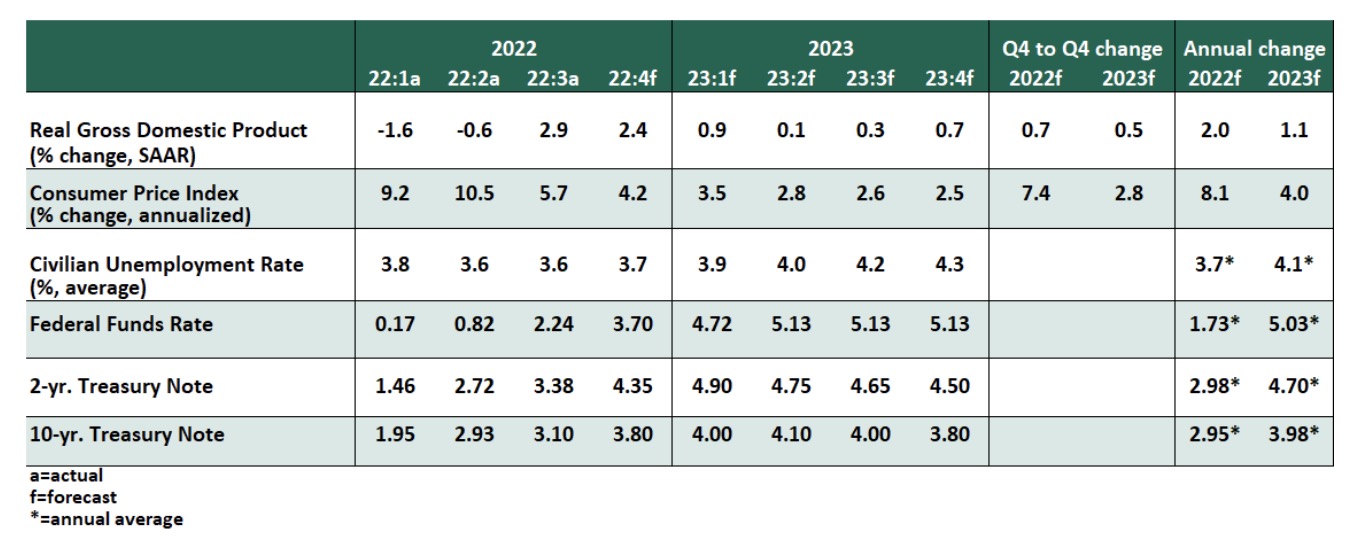

The Northern Trust Economics team shares its outlook for inflation, growth, employment and interest rates.

What's next for global growth? Our Macro Strategies team shares a regional breakdown of their growth expectations across the globe.

U.S. stocks are solidly lower as the markets continue to digest the economic implications of yesterday's 50-bp rate hike from the Fed.

In our 2023 outlook, we outline three key themes for the new year and highlight several implementation solutions investors can use to navigate potential challenges and grow client portfolios in the new year.

The latest adjustment snaps a four-month run of 75 bps interest rate increases by the Fed.

Andy Rothman explains the three reasons why he’s now bullish on China after being cautiously optimistic.

The Fed downshifted to smaller rate hikes but isn’t close to done.

Starting in 2012, it became more and more difficult for prudent dividend growth stock investors looking for income.

Democratization has become a buzz word within the fintech industry as technology and innovation have emerged to battle the headwinds that previously blocked accessibility to a subset of investment vehicles such as structured products.

In his latest memo, Howard Marks writes that the investment world may be experiencing the third major sea change of the last 50 years. Events in recent years – especially the spike in inflation and the Federal Reserve’s response – appear to have caused a reversal of the market conditions that prevailed after the Global Financial Crisis and for much of the last four decades. Howard discusses what this potentially new era could mean for lenders, especially bargain hunters.

Falling prices for cars and holiday discounting contributed to softer U.S. inflation, creating more room for the Fed to potentially dial back its hawkish stance.

Small-cap companies are usually the most vulnerable to volatility, with their stock prices and earnings getting hit particularly hard and early in economic downturns, much like what occurred in 2022. Yet they also tend to lead the way on both fronts during recoveries.

Yield is set to be a more important component of total return for investors during the next few years as the “Fed Put” exerts less influence on markets.

Emerging Markets (EM) assets were subject to three strong headwinds in 2022, namely, China’s zero Covid-19 and real estate crisis, aggressive interest rate tightening from the US Federal Reserve (Fed), and the Russia invasion of Ukraine.

The current market environment is attractive for a covered call strategy.

I was reminded in a recent read of Robert Hagstrom’s book, Warren Buffett: Inside the Ultimate Money Mind, how Warren Buffett and Charlie Munger define the economic earnings power of a business.

U.S. stocks are soaring in pre-market trading amid a softer-than-expected November consumer price inflation report.

The U.S. Superbubble, as Jeremy Grantham has termed it, featured the most dangerous mix of factors in modern times at the end of last year: all three major asset classes – housing, stocks, and bonds – were critically historically overvalued.

On his first visit to Japan since the pandemic, portfolio manager Shuntaro Takeuchi found new opportunities as well as familiar ones intact.

There’s a lot of chatter out there about recession…

The Fed’s mandate is stable prices and maximum employment.

Since the beginning of October, the market has performed better as a “Fed Pivot” bull case pushed investors into the market

Central banks are incurring losses.

As the super-growth cycle is ending in dramatic fashion, we are already seeing some of the most attractive valuation opportunities in years.

For the first time in a long time, muni investors may be able to earn attractive yields without having to take undue risk.

The recent escalation in interest rates is squeezing household budgets.