October will test the Fed’s resolve.

The fourth quarter is starting with a bang for precious metals markets.

The world seems an increasingly uncomfortable place for traditional stock and bond investments.

The latest jobs market headlines have been discouraging.

One of the themes I’ve discussed in recent months is the disconnect between a 40 year high in inflation and the lack of experience money managers have in understanding the monetary policy required to deal with such high inflation, including managers with 25 to 30 years of experience

For the last decade, central bank gold purchases have accounted for between 10% and 15% of total gold demand. George Milling-Stanley of SSGA takes a look at historical gold purchasing cycles over the past 50 years…

We are in the middle of a giant short squeeze, and it is going to get even bigger.

U.S. stocks are trading modestly lower in pre-market action with the markets awaiting tomorrow's key September nonfarm payroll report.

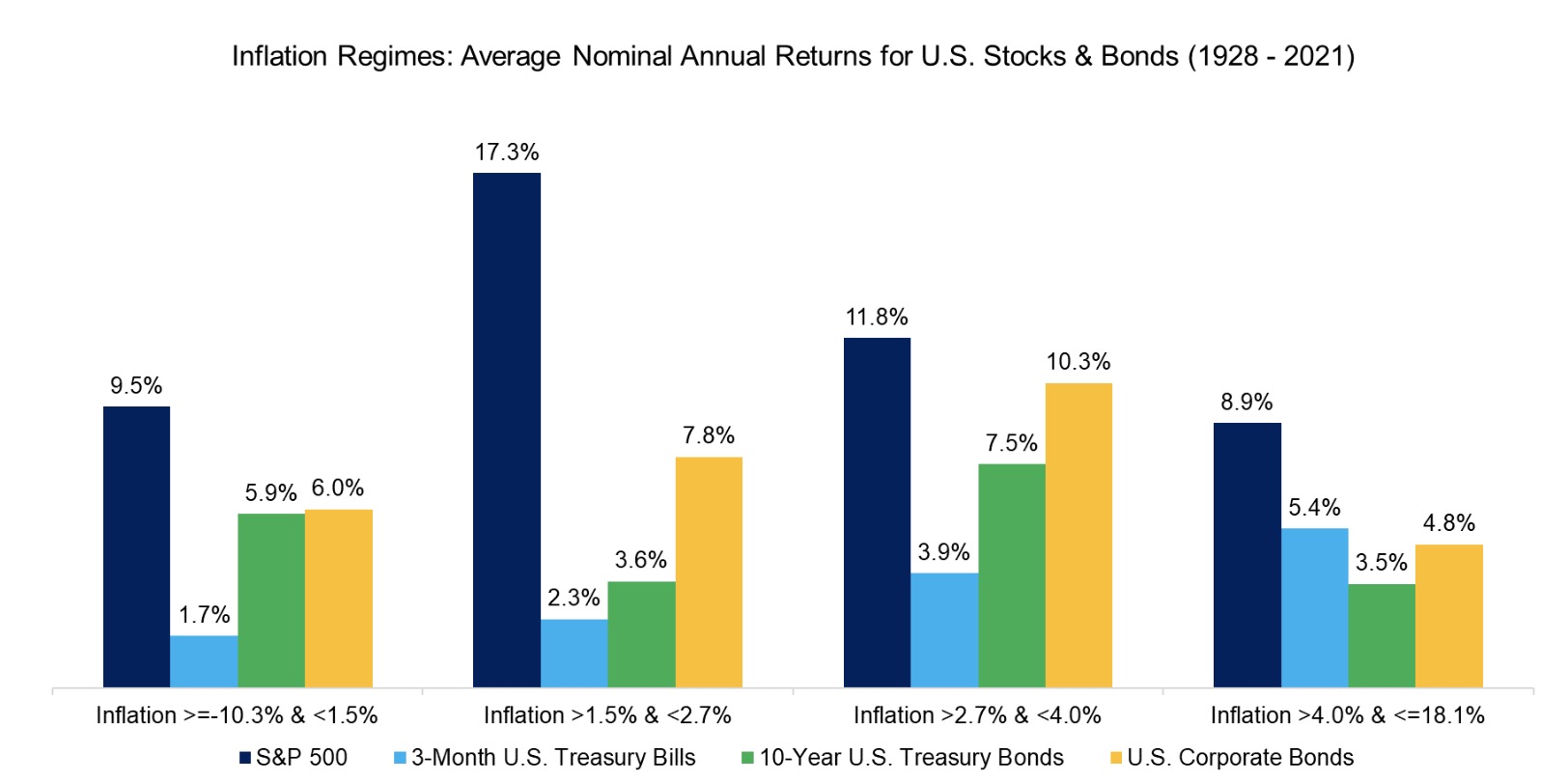

Many investors are searching for assets that can help protect portfolios from inflation.

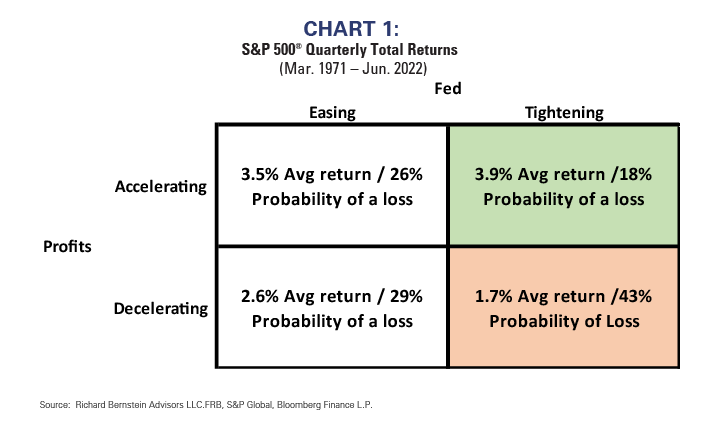

Rising rates hurt investors; claims on profits in the future are simply worth less if you discount them at a higher rate.

Bonds are typically considered safe investments. However, there were decades of negative real returns. Drawdowns reached 50% for U.S. Treasuries and Bonds.

Stocks extend yesterday’s gains as rates continue to ease.

As billions of fans eagerly await the 2022 World Cup, CIO Larry Adam draws parallels between the globe’s most popular sport and the current investing environment.

The list of assets that have risen year-to-date is both short and odd: energy, broad commodity indexes and the dollar.

After enjoying a long-running bull stock market, the recent drop in stock prices is causing investor angst.

Last night, the Reserve Bank of Australia stopped short of another 50bps hike to its overnight cash rate.

Equity market volatility persisted in the third quarter as investors came to terms with a new reality of high inflation and rising interest rates.

On August 16th, President Joe Biden signed the Inflation Reduction Act into law, ending months of uncertainty over whether congressional Democrats would ever reach agreement on a compromise budget reconciliation bill.

This is a critical time for investors and policymakers alike.

The investors of Smead Capital Management have been hearing us talk about ‘First World Problems’ recently.

Now that we are seeing much of this come to fruition, it is now time to turn the page to the next chapter.

In August, demand for bullion had slacked a bit from the frenetic pace set over the past two years.

We are not “recession deniers,” we just don’t think one has started yet.

A path remains in sight for the U.S. to avoid a recession.

We have a long and proud history of investing thematically and believe you can remove a great deal of volatility in your portfolio, if you do so.

Every time I cruise around Raleigh, it’s like Tesla drivers have multiplied.

The latest rate hike announcement by the Fed sent stocks tumbling to the year’s lows. While last week’s market action was brutal, the good news is the markets are set up for a rather significant short squeeze higher.

Generally speaking, when rates rise, so does the importance of investing in high-quality companies with strong operating metrics that can weather the higher cost of capital.

Just 18.5% of homes in Florida counties that were told to evacuate have coverage through the National Flood Insurance Program (NFIP), which is administered by FEMA. Most regular homeowners’ insurance policies don’t cover flood damage, which is why Congress created the NFIP in 1968. But at an average cost of $995 a year, according to Forbes, the insurance may be out of reach to many households.

This dark symphony was never going to end without sparking a currency crisis, one which allows countries to blame other countries as the source of their own internal problems. We will see that it’s not always the case.

Senior Sovereign Analyst Jon Levy looks at this week’s rate and currency shocks in the UK and shares what he believes is a root of the problem.

U.K. financial market volatility is likely to remain high, and the longer-term outlook likely depends on future monetary and fiscal policy.

Surveying the current condition of the financial markets, we presently observe a combination of still historically-extreme valuations, rising yet still only normalizing interest rates, measurably inadequate risk-premiums in both equities and bonds, and ragged, unfavorable market internals, suggesting continued risk-aversion among investors.

The massive debt levels provide the single most significant risk and challenge to the Federal Reserve. It is also why the Fed is desperate to return inflation to low levels, even if it means weaker economic growth.

Our last update was on August 26th and the market had peaked on the 16th of that month.

A number of key technical, sentiment and flow based indicators are suggesting we could see a relief in selling pressure over the coming weeks, and perhaps a countertrend rally in risk assets.

10 years have passed since the watershed year for pension risk transfer.

Over the last few months, the Federal Reserve (Fed) has changed its angle of attack quite dramatically, in an attempt to battle surprisingly and stubbornly high inflation.

“Gold is no longer a safe haven.” “Gold isn’t an effective hedge against inflation.” “Gold is dead.”

It’s been a tough year for investors, particularly in growth stocks.

It appears to us that global innovation has bottomed and offers attractive value.

Investors see a myriad of unknowns right now, and popular discussion continues to focus on a dichotomy between growth and cyclicals. We think there is a third choice that's being ignored.

U.S. equities are higher in afternoon action following a recent plunge to lows not seen since 2020.

Inflation remains persistently high, dominating everything else in the macro outlook.

In the midst of back-to-school season, David Mann opines on the real-life applications of mysterious middle-school math and exchange-traded funds.

In the 1980s there was a famous TV ad for Wendy’s with the tagline “Where’s the beef?”.

As the U.S. CPI data continues to rise, Charles Hamieh, Portfolio Manager at ClearBridge Investments, dives into the opportunity present for investors looking at the infrastructure space as an inflation hedge moving forward.

It’s easy to overlook the fact that, in thinking about investment risk, we are implicitly making a choice about the benchmark against which risk is measured.

After previously eschewing interest-rate hikes, the US Federal Reserve has been tightening monetary policy at an unprecedented rate.

Central banks haven't finished tightening and the U.S. Treasury yield curve remains inverted.