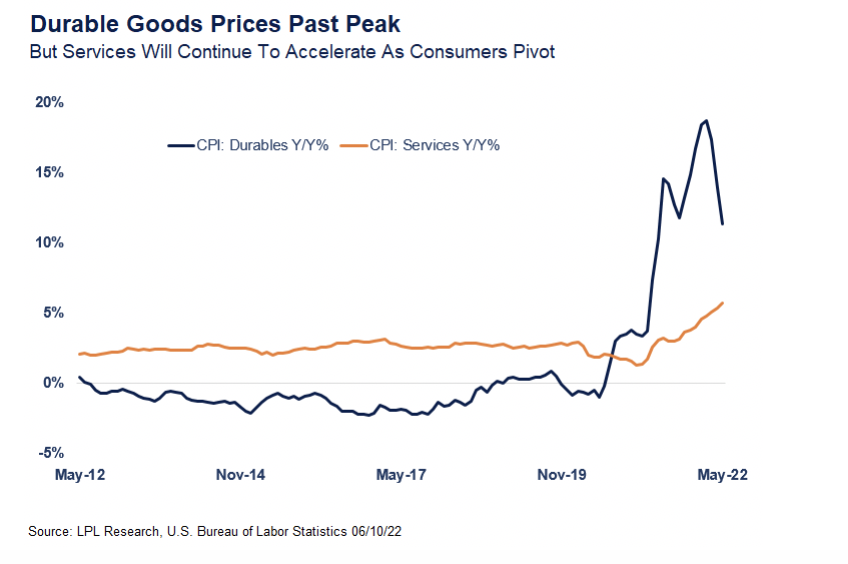

Headline inflation in May rose 8.6% from a year ago, accelerating from April’s 8.3% growth rate.

When will the bear market end?

Stocks modestly lower ahead of tomorrow’s inflation report.

Most investors take their cue from stock price volatility.

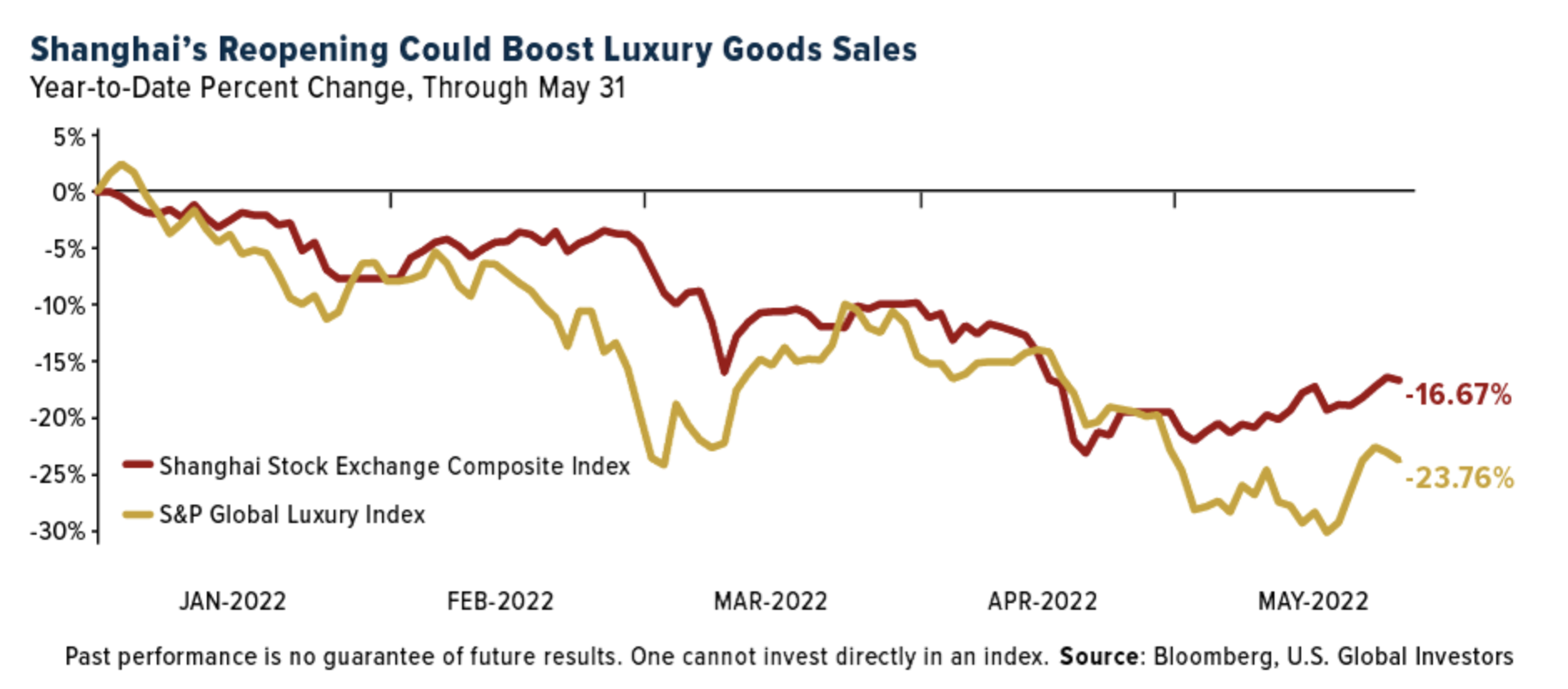

Shanghai, the Chinese commercial hub with 26 million residents, ended its two-month citywide pandemic lockdown last week, a sign that the world’s second largest economy may be ready to return to business-as-usual.

Crude oil and energy equities have been on a tear for the last two years.

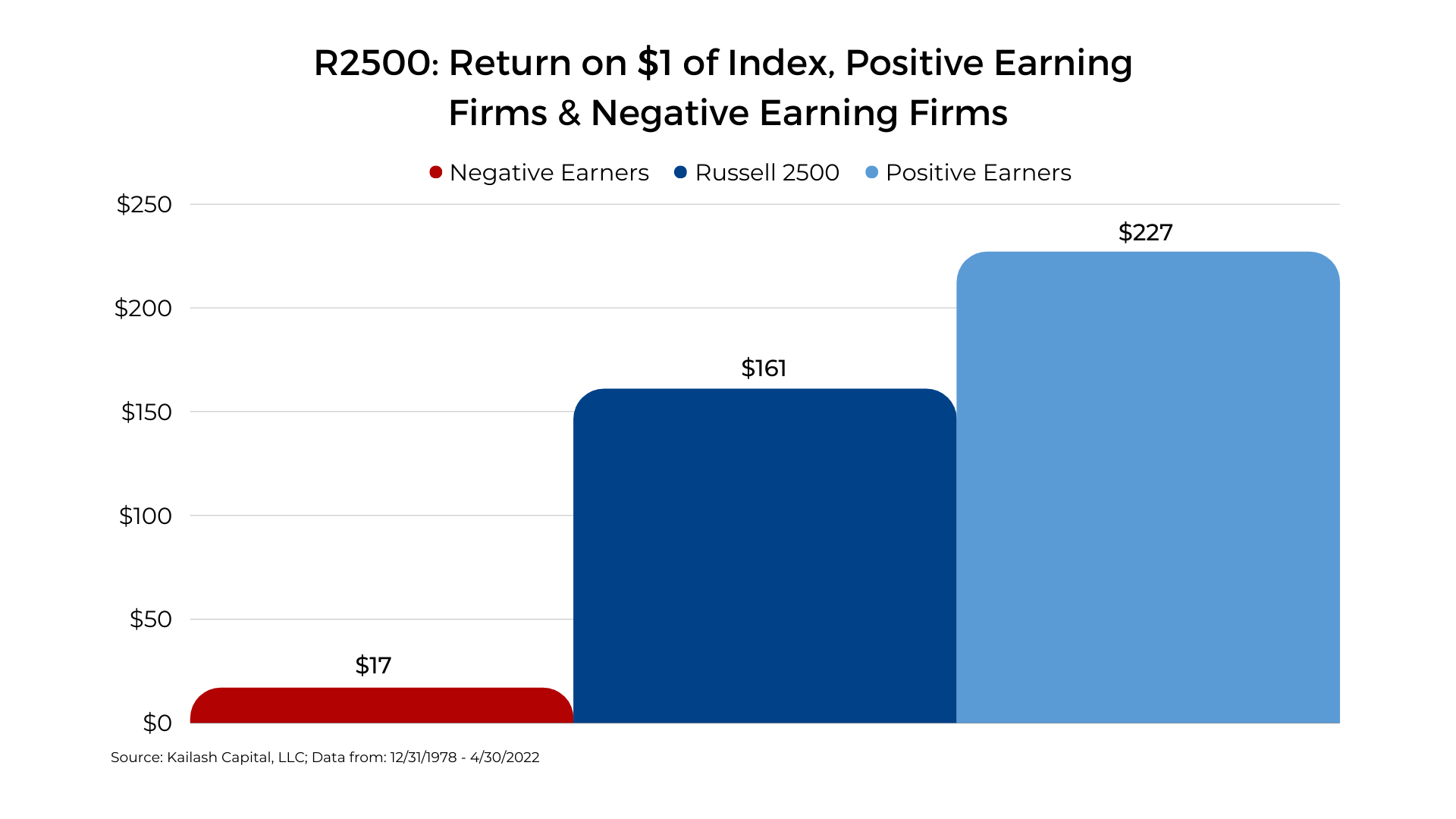

Not all value strategies have benefited equally during value stocks’ recent outperformance versus growth stocks.

How many billionaires are there in the United States?

Go around the world in one blog post; Loomis Sayles' Macro Strategies Group shares a visual snapshot of its GDP growth expectations for the months ahead.

Investor sentiment expert Peter Atwater believes the bear market is only just beginning.

Howard Marks’s latest memo explores recurring investment themes to contextualize the current market correction and the bull market that preceded it. He discusses the role played by financial innovations like SPACs and cryptocurrencies and why he believes psychology, not fundamentals, primarily drives investment cycles – and likely always will.

The ECB and the Fed both need to quickly normalize policy from the emergency settings adopted when the pandemic first hit.

Japan zero-inflation mindset is no match for today's price pressures.

The most recent change on the supply side of the global oil market has involved Saudi Arabia suddenly and dramatically regaining its swing-producer role.

Gold and silver is money. Everything else is credit.

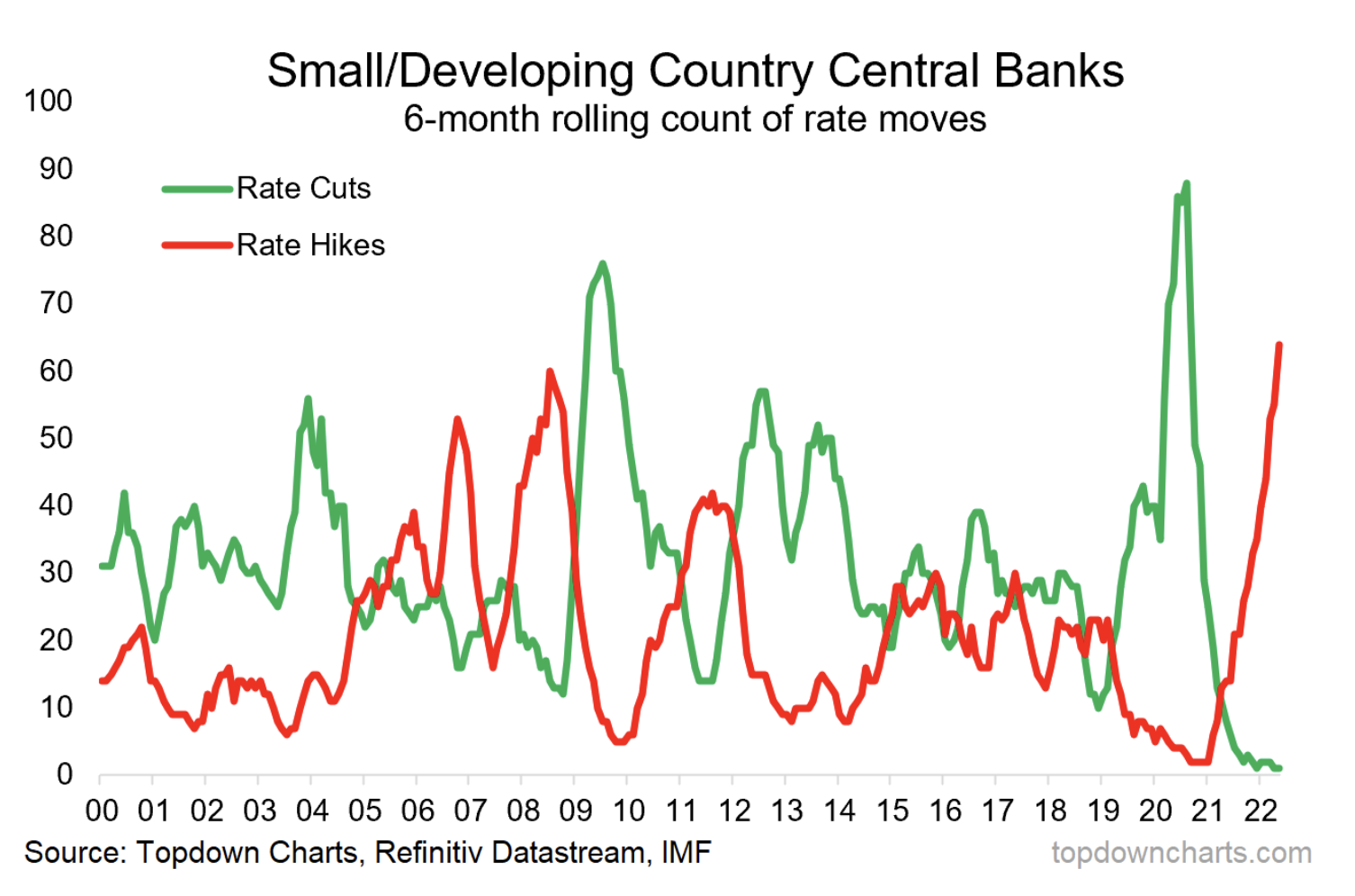

This is one of my favorite charts, and one that helped get us onto the right side of the global policy pivot that has rippled across markets this year.

Academics argue that there are three proven factors of investing: Value, quality and momentum.

On the latest edition of Market Week in Review, Director of Investment Strategies, Shailesh Kshatriya, and Director of Institutional Investment Solutions, Greg Coffey, discussed the recent PMI (purchasing managers’ index) readings from China and the U.S.

A cooler housing market isn't a bad outcome.

U.S. equities are lower as the recent volatility continues despite yesterday's gains.

Thoughts on recent market volatility and implications for investors from Head of Franklin Templeton Institute, Stephen Dover.

JP Morgan CEO Jamie Dimon caused a stir lately when he talked about a "hurricane" hitting the US economy.

We are excited to start sharing the thought process of Erlanger Research on Advisor Perspectives as perspectives and unique views are something that there is no shortage of in our shop

Absent a crisis, stiffer regulation of cryptocurrencies could take many decades, especially given that major players are pouring huge sums into lobbying.

Investors are shifting their focus from runaway inflation to slowing global growth as central banks hike rates to tame price pressures.

We have a very precise methodology for dissecting the world’s equity markets.

Strong employment and spending will help the economy grow through current shocks.

Will the Fed pause its rate hikes as markets correct?

LPL Research looks at the May jobs report and its impact on markets and Federal Reserve (Fed) policy.

Let me take a minute to introduce myself and my publication The FRED Report.

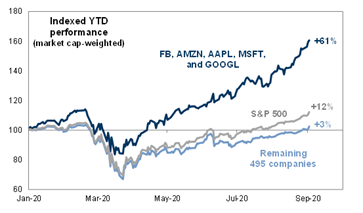

It’s not all doom and gloom, though. Due to stratospheric oil and gas prices, energy stocks have been the one bright spot in an otherwise dour market this year. Through the end of May, the S&P Oil & Gas Exploration & Production Index gained an incredible 60%, compared to the S&P 500, which fell about 13%.

The chance that all the necessary pieces will line up that way? Somewhere between slim and none, and as my dad used to say, “Slim left town.” And while my memory isn’t perfect, I don’t believe any speaker at the conference believed in the possibility of a soft landing. And even if we get one, we have serious problems that predate this inflation. They haven’t gone anywhere.

Is a “lost decade” ahead for markets?

Markets stabilized in May after one of the worst months since the start of the pandemic.

In January Goldman Sachs projected that the FOMC would increase the federal funds rate at every other meeting (each meeting is 6 weeks apart) starting with the March meeting.

Bear markets always signal a leadership change within the overall equity market. The leadership going into a bear market is rarely, if ever, the leadership coming out. Because of this rule of thumb, we view bear markets as periods of extreme opportunity.

Sharp, countertrend rallies may continue this year, but aggressive Fed policy, the turning of the liquidity tide, and slower economic growth will likely keep pressure on stocks.

Welcome to another subscriber request where I will cover 42 stocks.

We strongly believe that the traditional benchmark-led approach to investing in emerging market debt can be far from optimal.

This commentary provides a look at what we covered in the latest Weekly Insights report. The Weekly Insights Report is part of our entry-level service: presenting some of the key findings from our institutional research service.

Virtual reality is not reality!

The first half of the year has so far been challenging for investors in municipal bonds.

A fascinating aspect of the financial markets is that long-term returns are driven almost entirely by math, while short-term returns are driven almost entirely by psychology.

Municipal bonds acquired at too deep a discount could be subject to an additional tax, known as the de minimis tax, which would take a bite out of the after-tax return.

Markets flailed in May, seeking certainty amid conflicting signals.

There are eight global mountaintops scaling 26,000 feet or higher, including Mt. Everest, the most famous of them all.

Through rising real yields, a slowing economy and poor seasonality, short-term headwinds remain for gold and precious metals.

For the year ending December 31, 2021, passive mutual funds and ETFs reported estimated net inflows totaling $958.43 billion, compared to estimated net inflows totaling $249.91 billion for actively managed funds.

We are now about five months away from the mid-term elections that will decide who controls the Senate and House of Representatives for the next two years.

Has the global investment environment which we have grown accustomed to over the past few decades fundamentally changed?