Inflation and hawkish central bank talk have spooked investors and led to bond losses not seen since the 1980s in developed markets (DMs).

In this video you will see dividend growth stocks, some that remain overvalued, some that have become undervalued and everything in between.

The economy seems to be doing well, with job growth still at high levels, consumer spending still healthy, and businesses continuing to invest.

With luck, the risk of a synchronized global downturn will recede by late 2022.

With the world economy still recovering from the COVID-19 pandemic and now dealing with the Ukraine-Russia crisis, markets face a great deal of uncertainty.

Stock prices and bond yields have been moving in opposite directions this year.

With France’s polls closing yesterday Emmanuel Macron will now serve a second consecutive term as the president of France, the first to do so since Jacques Chirac in 2002.

Disaster is a strong but appropriate word that applies perfectly to the state of U.S. monetary policy.

U.S. stocks fell Friday, extending a run of weekly losses into its third straight week, as investors reacted to a handful of disappointing earnings reports and the Federal Reserve’s increasingly aggressive language about future interest rate increases.

Stanley Black & Decker has increased their dividend for 54 consecutive years making it a Dividend Aristocrat, Dividend Champion and a Dividend King.

The dollar is not as dominant as it was two decades ago, but is still the leading global currency.

No one can say that the Federal Reserve can't do the impossible.

While recent shocks have made the current inflationary surge and growth slowdown more acute, they are hardly the global economy’s only problems.

Is there a bear market lurking in the shadows?

Through higher mortgage rates, demand for US housing is beginning to wane.

On May 29, Colombia could elect its very first leftist president should Gustavo Petro receive a majority of the vote. The former congressman and mayor of the capital city of Bogotá, Petro is an unabashed admirer of and Hugo Chávez.

If you haven’t noticed—perhaps because you live on Mars—inflation is here. Not just in the US but almost everywhere. Prices for everyday goods and services, including necessities like food, are climbing rapidly. The US Consumer Price Index rose 8.5% in the 12 months through March… and we know it understates categories like housing.

Chief Economist Scott Brown discusses the latest market data.

It might seem at first that everything is against emerging markets.

High-yield bonds have a reputation for volatility.

When reviewing the current state of the global economy and investment markets, we recommend focusing on market signals and weeding out market noise.

The International Monetary Fund’s significant downward revision to its 2022 World Economic Outlook, just one quarter into the calendar year, has generated headlines and hand-wringing around the world.

Concerns about the Ukraine war, inflation, and the Fed were top of mind last quarter, but a lesser appreciated long-tern headwind is the de-globalization of the labor force, which could have profound effects on the economy.

Our last edition of Volume Analysis stated, “The federal reserve’s rocket has since overshot its orbit, causing massive inflation while providing a speculative paradise for risk assets.

Even though Netflix (NFLX) stock is down approximately 35% today, I contend the company is still too expensive to invest in.

Despite gloomy news out of China, Andy Rothman explains why he remains optimistic about China’s road ahead.

The clear and present danger to the global economy is inflation because global central banks are starting to take aggressive actions to deal with what they now believe to be non-transitory inflation.

I didn’t start the fire.

For US states, spring marks budget season, a time to check the ledger board and allocate funds to entities and projects within the state—or cut back where needed.

Interest rates are structurally set up to go higher.

Traditional long-only fixed income managers had one of the worst quarters on record in Q1 2022 as higher interest rates left “bottom up” portfolios overweight duration.

Real Treasury bond yields fell into deeply negative territory in 2021.

Although inflation has risen sharply for multiple reasons, increased demand is by far the most important factor.

Is it still a “bear market rally?”

As a result of the recent bear market action in stocks, many have fallen to 52-week lows.

The Northern Trust Economics team shares its outlook for key markets in the month ahead.

An often overlooked and underutilized fixed-income alternative, preferred securities offer investors compelling diversification and income opportunities in today's volatile, rising interest rate environment. With yields and returns comparable to high-yield fixed income, today's preferred securities have evolved into a distinct and attractive income-generating asset class.

As we have noted in this space in the past, there is a lot of the world that cannot be captured by the most elegant and detailed of spreadsheets.

Five commercial real estate sectors in markets across the globe have the potential to thrive in this environment.

Russia’s invasion of Ukraine has exacerbated inflation, which was already rising. The big questions now are how far will the Fed be willing to go to slow inflation, and how will the market react as rates increase?

Something in the market changed about a half-year ago. A dandy old “truism” that had made the rounds for ages got scrapped.

Recession chatter has picked up increasingly for numerous reasons, not least being the spike in oil prices, slowdown in economic growth estimates, and the Fed's transition from accommodative to tighter monetary policy.

The war in Ukraine has further complicated the investment backdrop, and fears of a recession are rising now that the U.S. yield curve has inverted. Given so much uncertainty, we are focusing on what we can control and maintaining a defensive posture

Real GDP, in the US, grew 5.5% in 2021, the fastest growth for any calendar year since the Reagan Boom in the mid-1980s.

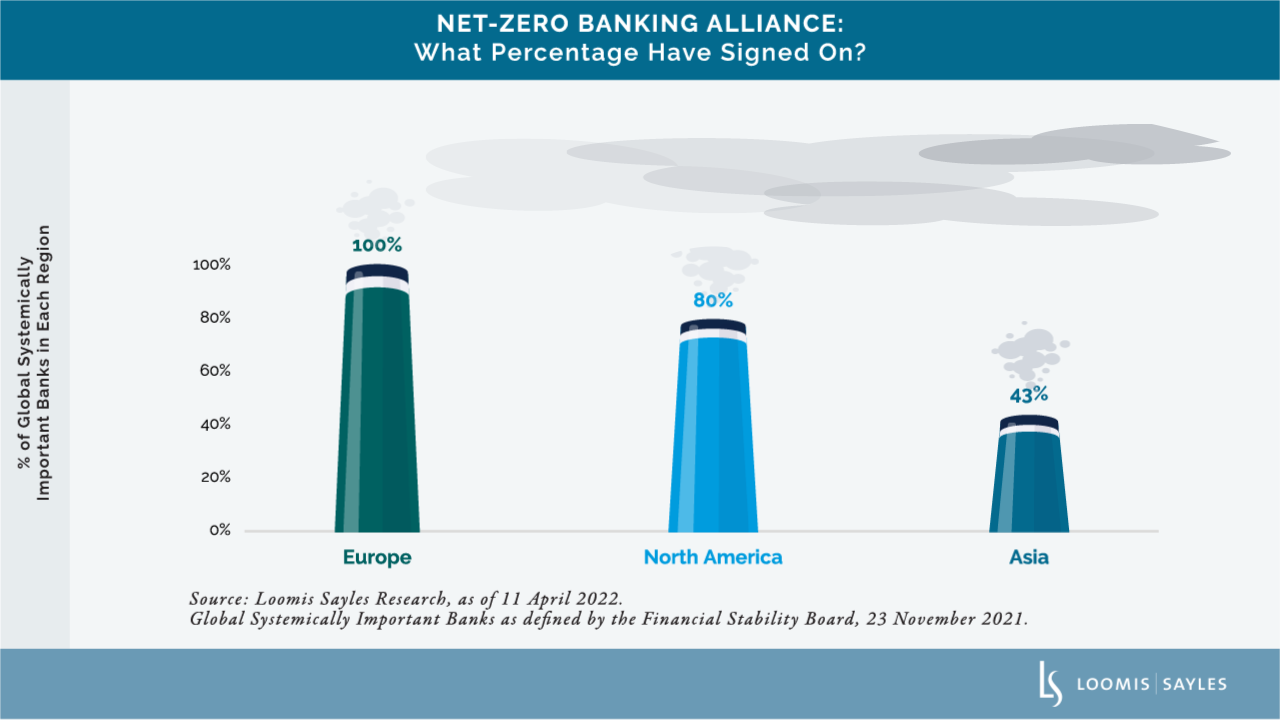

Senior Global Equity Opportunities Analyst Julian Wellesley looks at the progress banks have made in disclosing their climate risks and how they could still improve.

The “wisdom of the crowd” isn’t always wise to follow. A recent article by Scott Nations via MarketWatch made an excellent point.

Moving forward beyond the pandemic of 2020, the theme the world woke up to is that people want more…more home, more land, more entertainment, more goods.

The countries’ weight in global trade is relatively small, but outsize exports of raw and semi-finished goods may portend price hikes across a variety of industries.

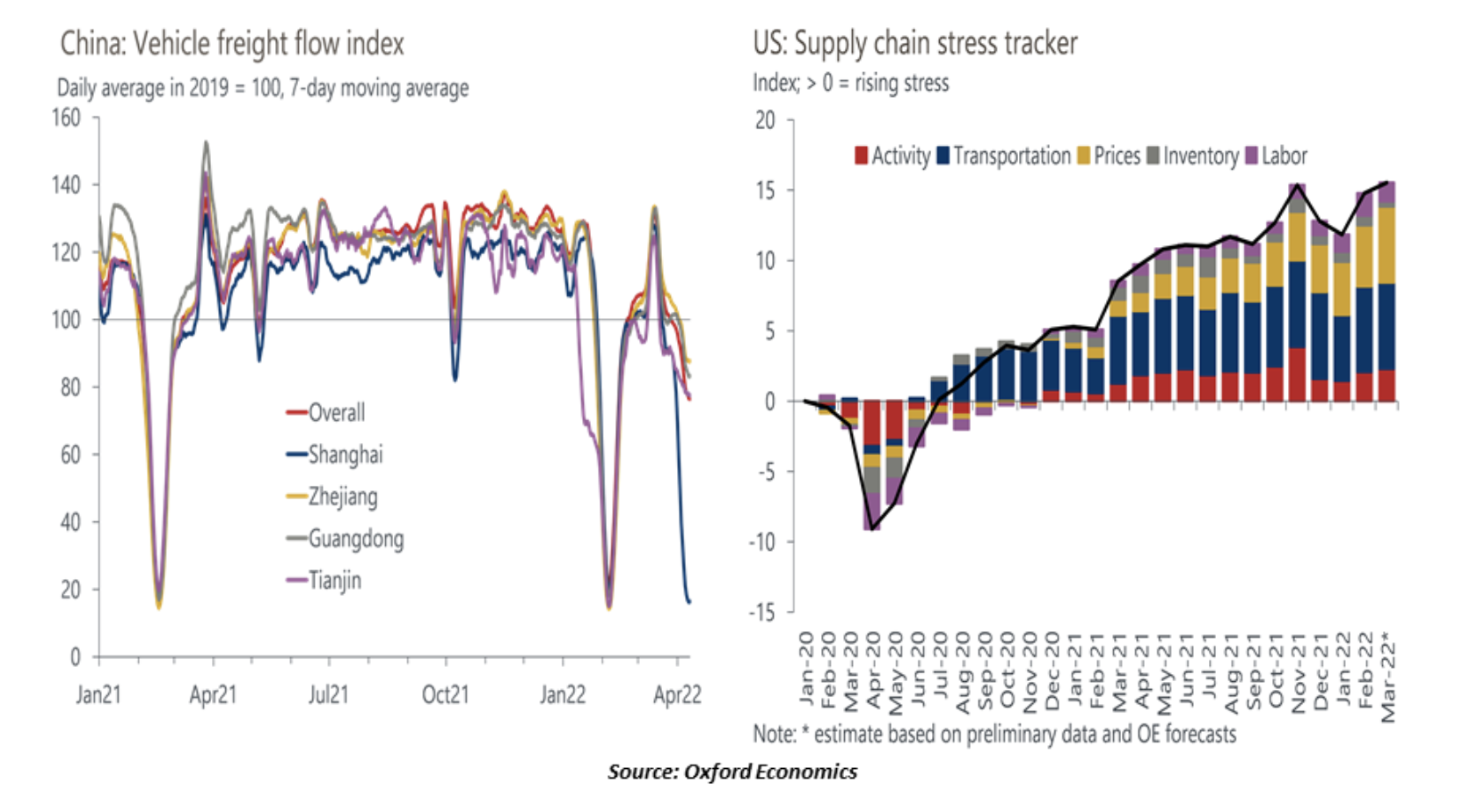

China's zero-COVID approach will undermine its position as the supply chain hub of the world.

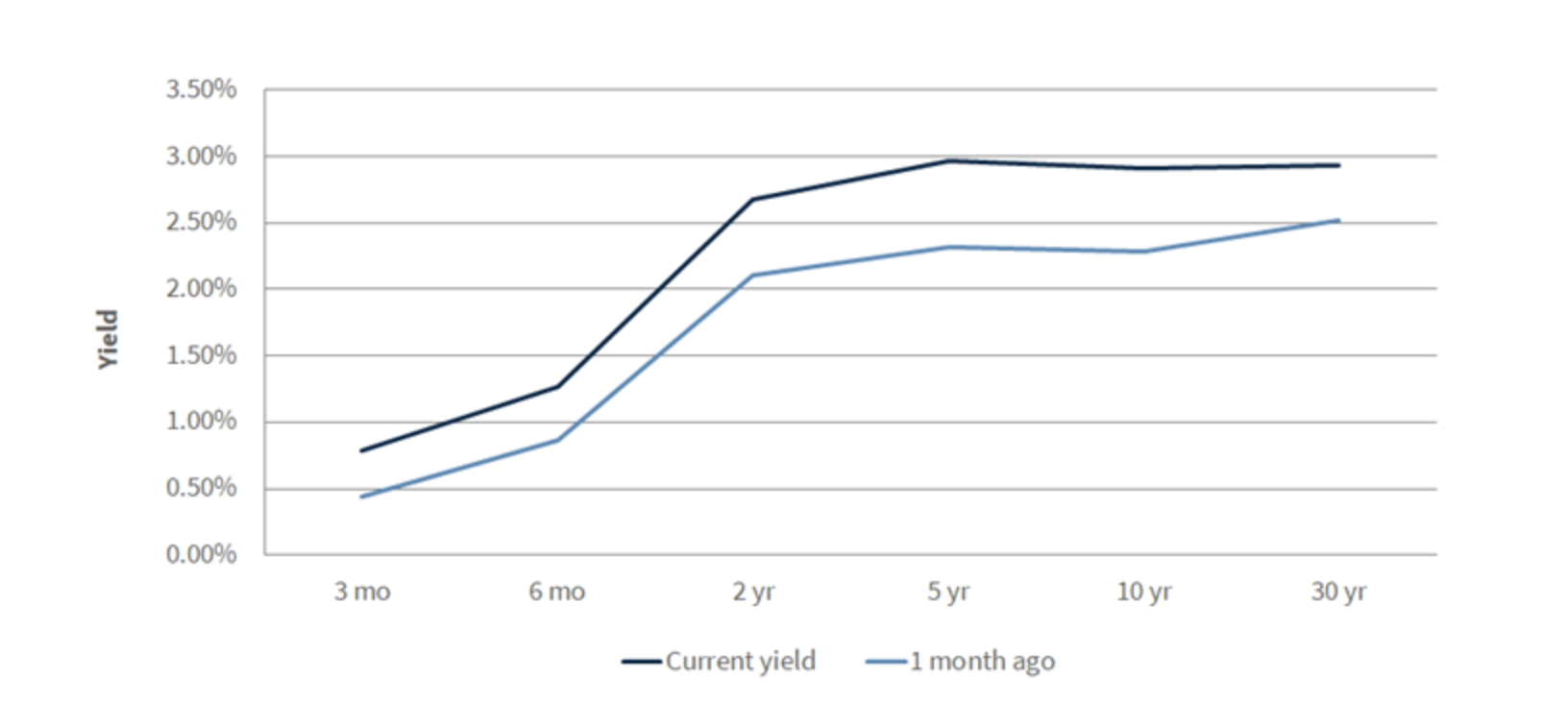

It’s Easter weekend, so we are going to revisit a 2018 letter about the yield curve. The yield curve is much misunderstood and misused by many analysts. This letter will give you the tools to understand the correct importance and relevance of the yield curve. And then, a few comments about Ukraine.