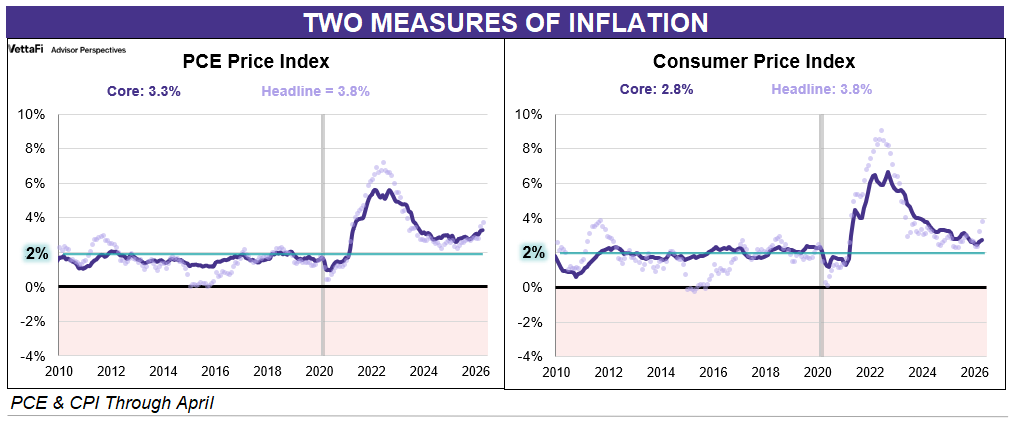

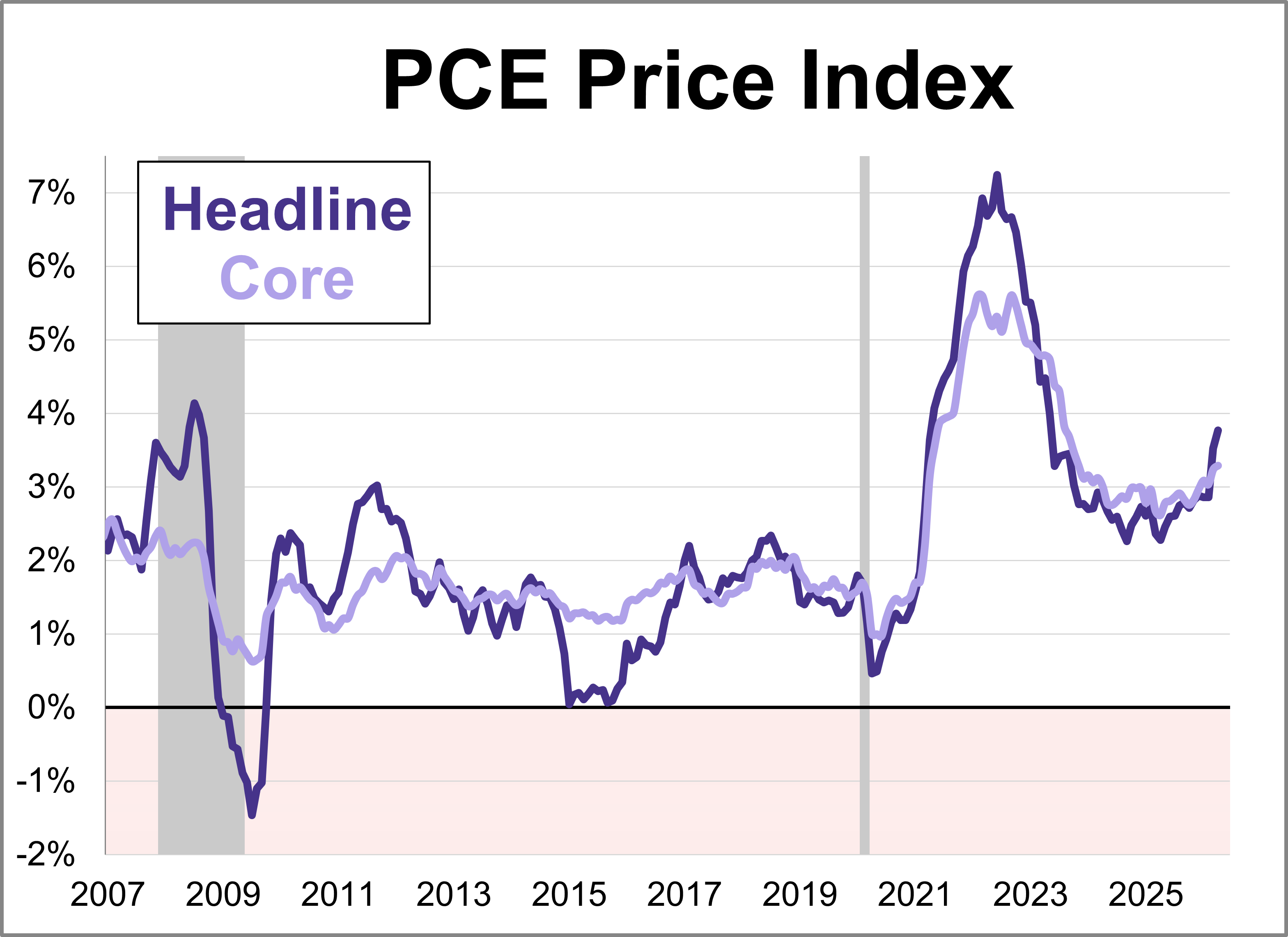

Inflation remains a hot topic, directly impacting everything from your grocery bill to interest rates. As of the latest data, two key inflation gauges — the Personal Consumption Expenditures (PCE) Price Index and the Consumer Price Index (CPI) — show that prices are still above the Federal Reserve's 2% target, with the core PCE at 3.3% and core CPI at 2.8%.

Personal income (excluding transfer receipts) was down 0.05% in April and was up 2.68% year-over-year. However, when adjusted for inflation using the BEA's PCE Price Index, real personal income (excluding transfer receipts) was down 0.44% month-over-month and down 1.04% year-over-year.

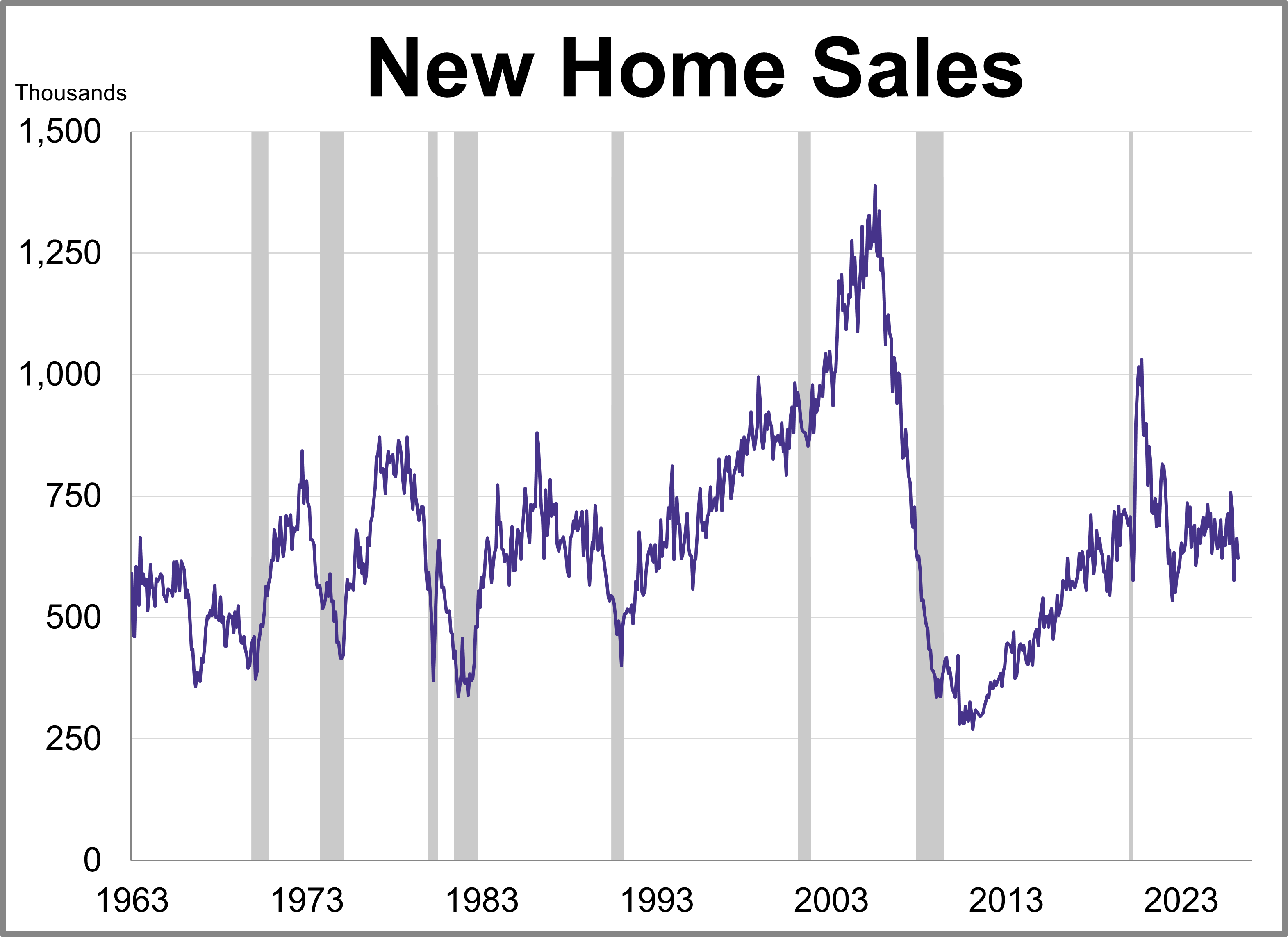

New home sales fell more than expected in April while the median price experienced its largest jump in seven years.

Treasuries rallied back to be little-changed on the day, erasing earlier declines spurred by higher oil prices, after a key US inflation gauge rose less than expected.

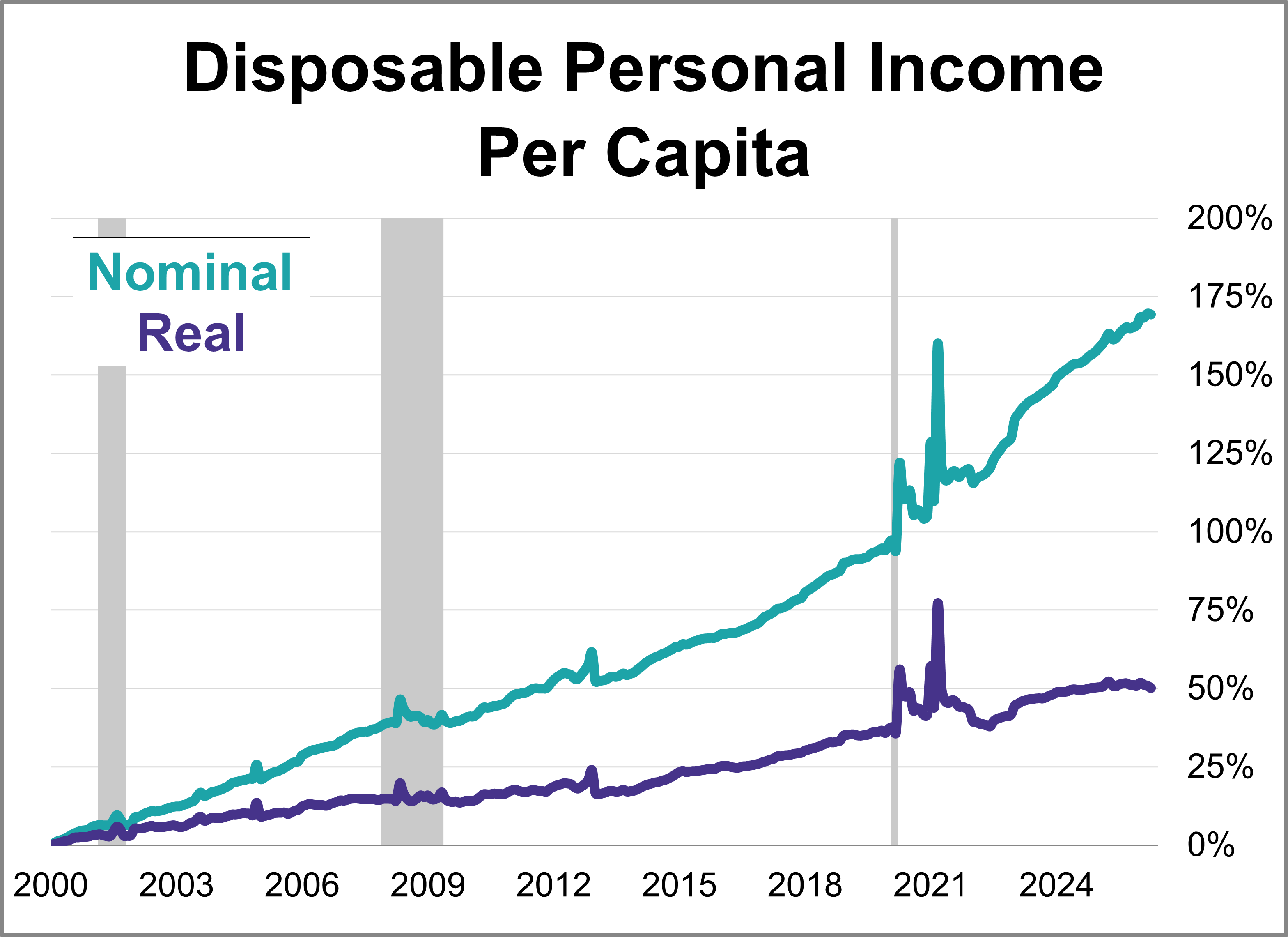

With the release of April's report on personal incomes and outlays, we can now take a closer look at "real" disposable personal income per capita. To two decimal places, disposable income per capita was up down 0.10% month-over-month. But when adjusted for inflation, real disposable income per capita was down 0.50%.

Shares of retailers spanning Kohl’s Corp. to Best Buy Co. and Dollar Tree Inc. rose on Thursday amid optimism that shoppers are still spending when they see what they want at the right price.

An abundance of cash in US funding markets appears to be driven by deeper structural shifts that are unlocking billions of dollars in balance-sheet capacity at the biggest banks, Wall Street strategists say.

Coverage of prediction platform Polymarket has recently converged on a single statistic, delivered with the cadence of a verdict: Most users lose money. The top 1% of accounts capture roughly three-quarters of the gains, while most traders since 2022 are underwater.

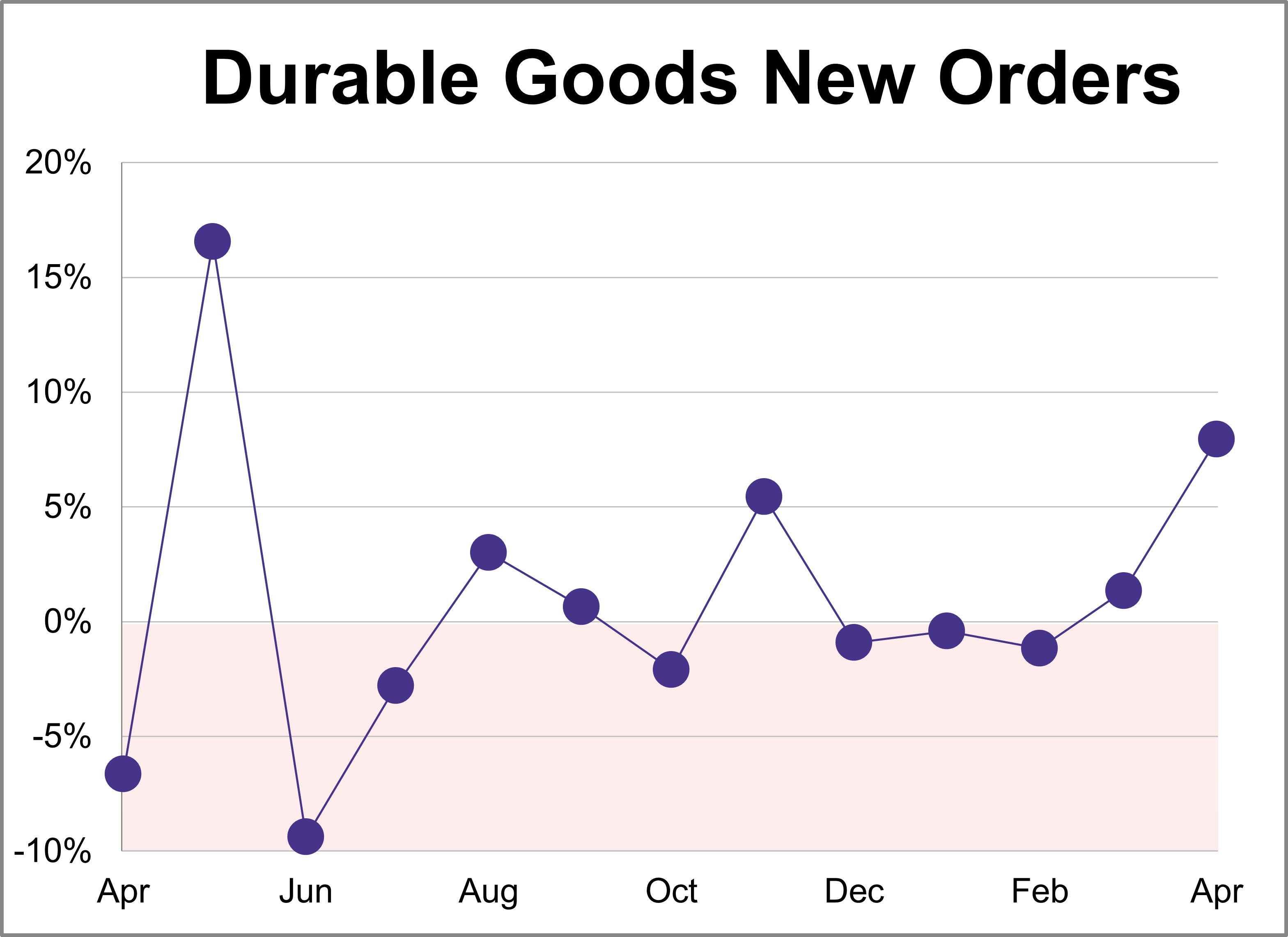

New orders for manufactured durable goods jumped 7.9% in April to $345.96B, almost twice as much as the projected 4.0% monthly growth.

Bankers are preparing to sell a jumbo debt package to support the $110 billion acquisition of Warner Bros. Discovery Inc. It’s a risky deal and comes at a moment when the bond markets have been wobbling.

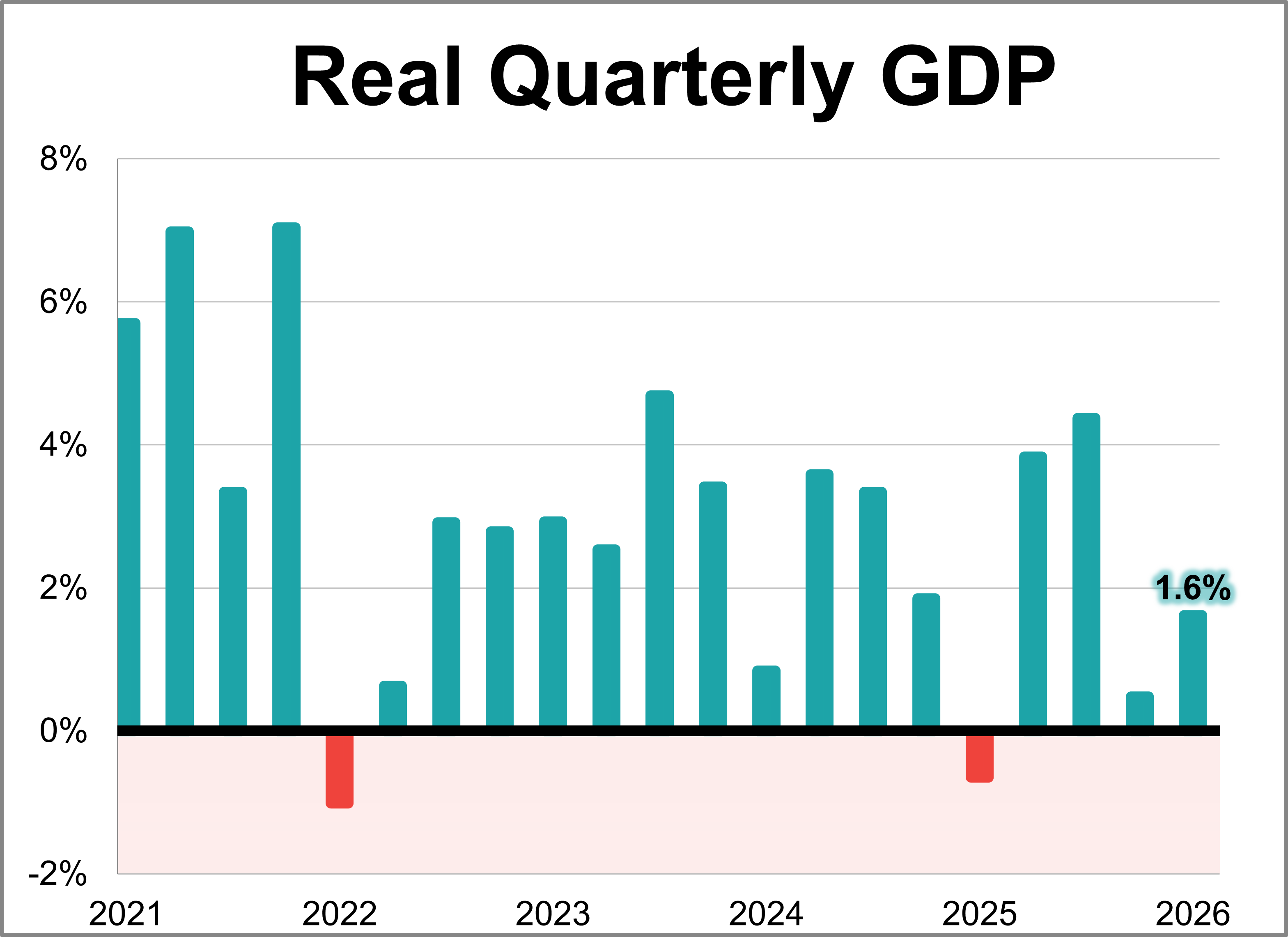

U.S. economic growth rebounded at the beginning of 2026, according to the BEA’s latest estimate. Real GDP rose at 1.6% annual rate in Q1, falling short of the 2.0% forecast but marking an acceleration from the 0.5% final estimate seen in Q4 of last year.

The Federal Reserve’s preferred inflation gauge, the core PCE price index, climbed 3.3% year-over-year in April. This marks the highest level since November 2023 and marks a steady pickup from March's 3.2% reading. On a monthly basis, core prices rose 0.2%.

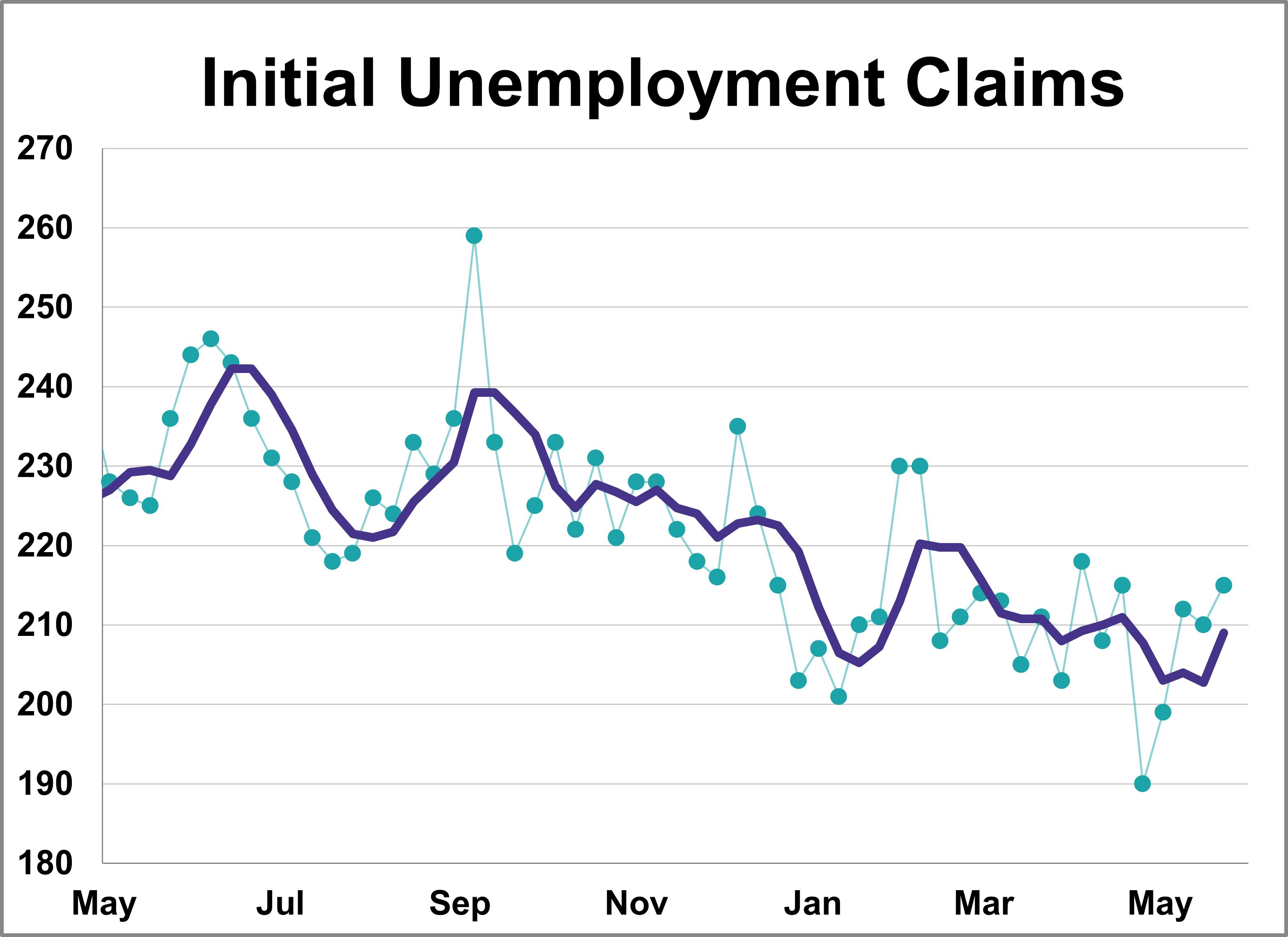

In the week ending May 23rd, initial jobless claims were at a seasonally adjusted level of 215,000. This represents an increase of 5,000 from the previous week's figure and was higher than the forecast of 211,000.

In a relatively light week for traditional economic data, a mix of corporate earnings, business surveys, Federal Reserve minutes, and the latest read on the consumer from the University of Michigan helped paint an increasingly clear picture for investors.

The push for international equities diversification continues amid shifting global macroeconomic conditions. These days, investors have more options when it comes to international exposure. Given the current market uncertainty, they may want to put quality at the forefront of their decision-making process.

It’s the first word that comes to mind to describe Q1 2026 U.S. company earnings. S&P 500 earnings growth is looking set to reach 28% year over year (yoy), more than double the consensus estimate of 12% at the start of the reporting season.

The artificial intelligence (AI) boom has transitioned from an equity market narrative to a defining force in fixed income. Hyperscalers (Amazon (AMZN), Alphabet (GOOG/L), Meta (META), Microsoft (MSFT), and Oracle (ORCL)) are shifting from internal cash flows to substantial bond issuance to fund massive data center, graphics processing unit (GPU), and power infrastructure buildouts.

Thanks to strong gains in markets over recent years, the 60/40 default portfolio has quietly morphed into a bundle of expensive U.S. growth equities and credit exposures offering narrow spreads over Treasuries.

Contrary to what legal television series portray, verdicts rarely turn on a single moment of drama. They take shape gradually, as evidence accumulates and a broader narrative comes into focus.

US growth stocks underperformed in early 2026 amid AI disruption fears and an unresolved conflict in the Middle East. But these stresses could create favorable conditions for selective, diversified investors to unlock long-term growth potential in a rotating market.

Goldman Sachs Asset Management (GSAM) made a big announcement this week, touting $100 billion in total ETF AUM. The milestone comes following the firm’s recent acquisition of Innovator ETFs adding several notable funds to the firm’s overall roster.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

After three decades of watching market cycles play out from both sides of the trade, I’ve come to a simple conclusion: Wall Street’s love of simple rules is one of the most dangerous aspects of investing.

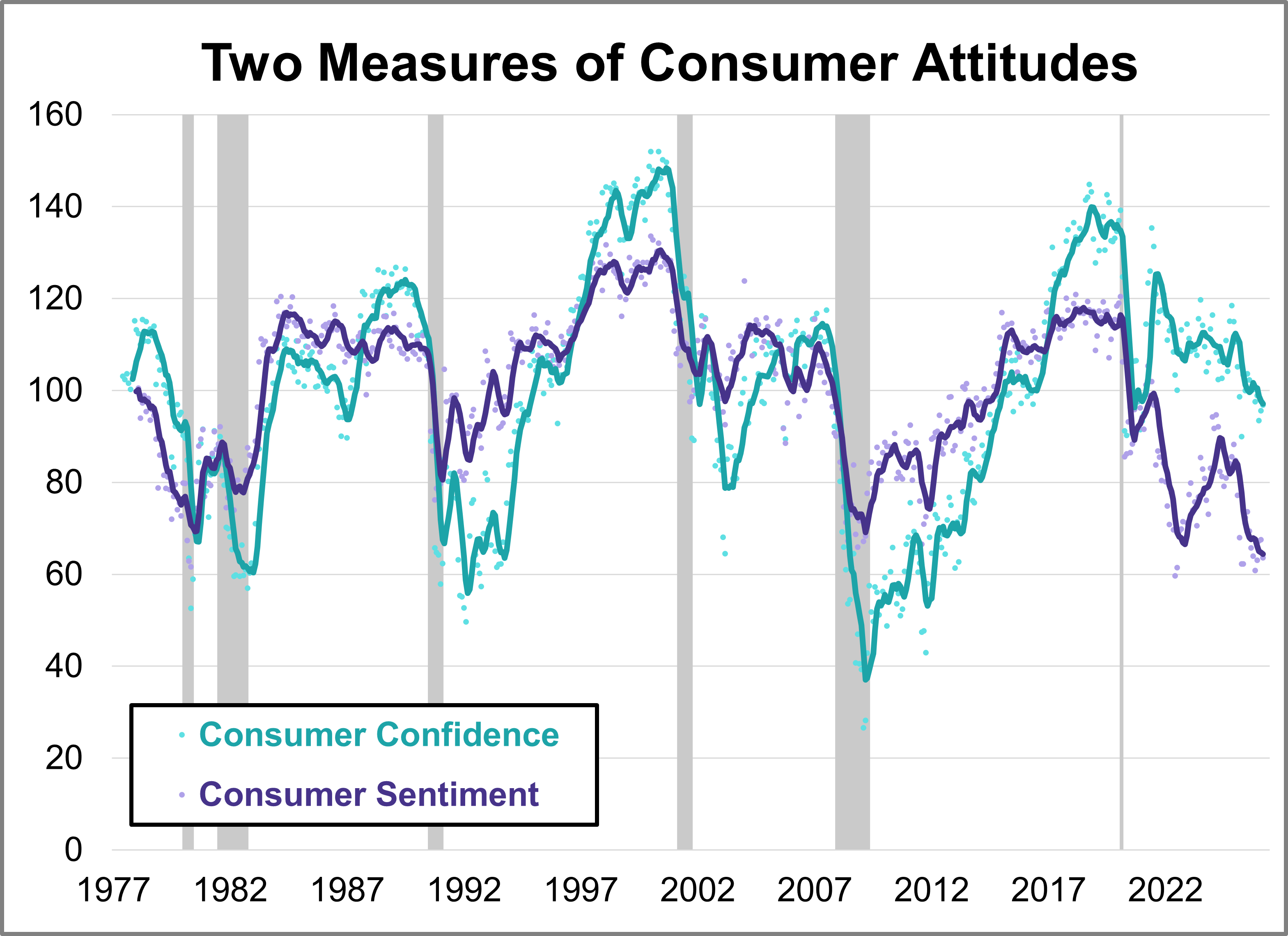

What are consumers thinking about the economy? Their collective mood offers crucial clues for businesses, investors, and policymakers alike. In May, the two leading benchmarks, the University of Michigan’s Consumer Sentiment Index (MCSI) and the Conference Board’s Consumer Confidence Index (CCI), offered similar views with both retreating amid ongoing inflation concerns.

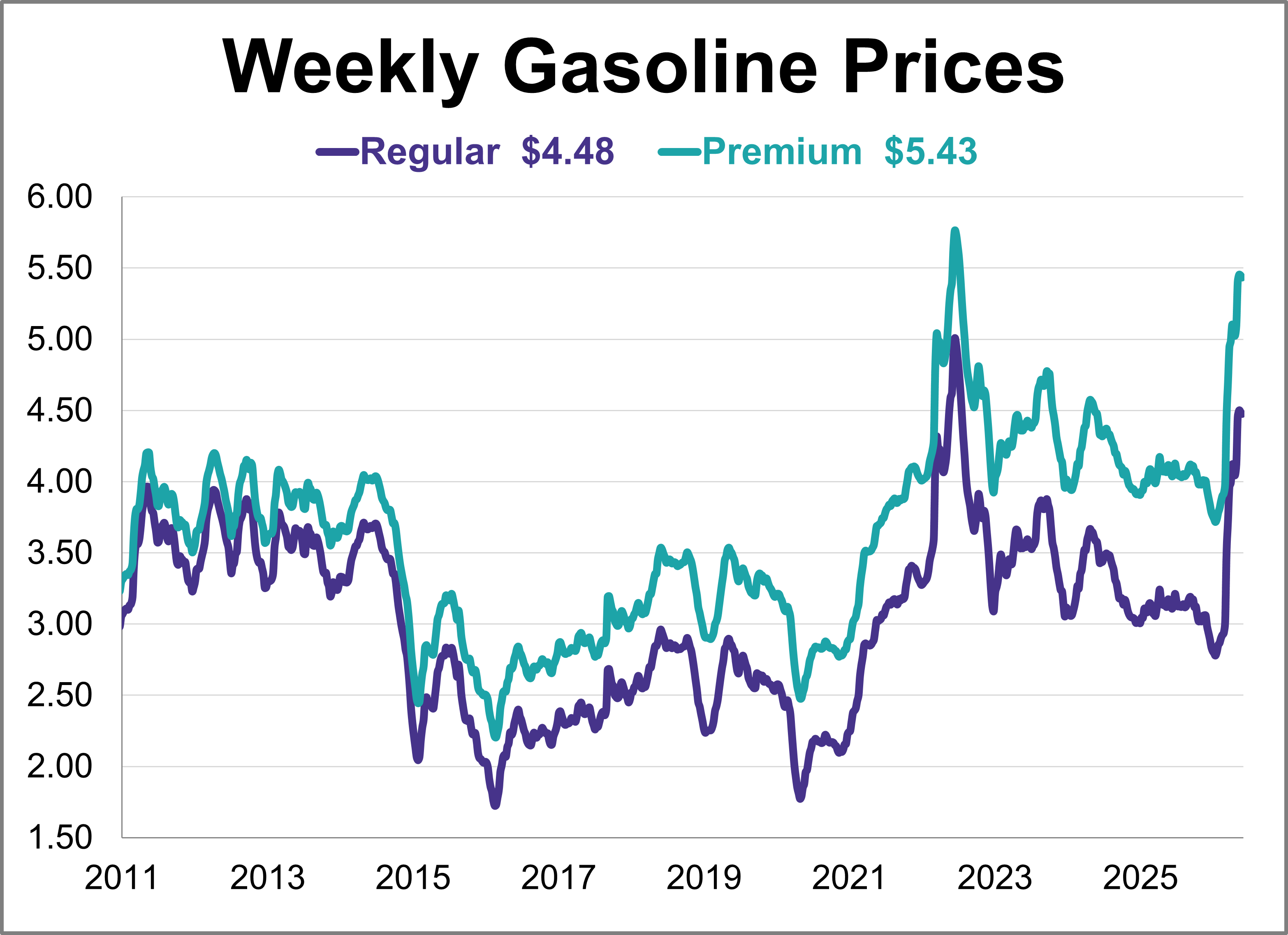

Gas prices inched lower for a second straight week though remain near their highest level in almost four years. As of May 25th, weekly prices were down 2 cents for regular and premium gasoline.

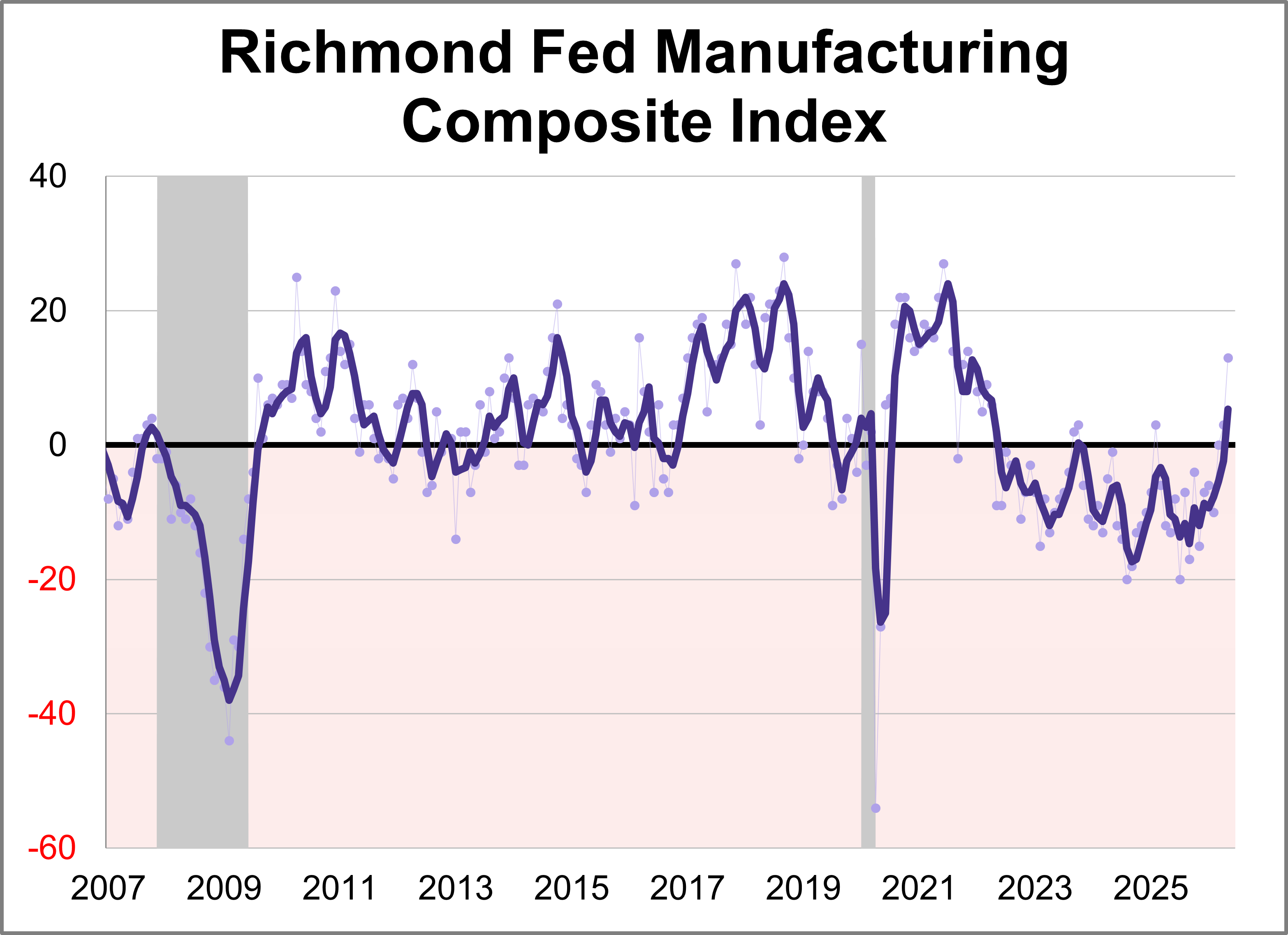

Fifth district manufacturing activity increased in May according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose ten points points to 13, marking the highest level in nearly five years. This month's reading was above the forecast of 4.

Advisory firms need tighter integration between their daily work tools and the CRM at the center of their world. When notes sit siloed from the rest of a firm's data and operations, the chance to deepen team collaboration and sharpen client insights goes with them.

Leading with bad news can feel wrong and even confrontational at some level, but the psychology research supports it, the behavioral finance supports it, the career math supports it, and the clients who stay through multiple cycles apply the final confirmation stamp.

Some people do much better with change than others. It isn’t that they can’t change or they actively resist it. Rather, they experience more fear, more concern and they need more clarity about what the change means to them.

Private credit is more inherently complex than the traditional bond market. In comparison, private credit information comes at a deficit. That’s because private credit loans are essentially bespoke agreements between a lender and a private borrower.

The breakneck surge in memory-chip stocks is intensifying, sending the market capitalizations of SK Hynix Inc. and Micron Technology Inc. above $1 trillion for the first time, as investors bet the AI boom will lead to a sustained revaluation of the industry.

Despite the pickup, India’s municipal paper still makes up for less than 1% of the total rupee bond sales. By comparison, the segment represents 7% of the overall bond market in the US, according to CareEdge Ratings’ January report.

Almost two-thirds of fund managers permit some level of “nuclear exposure,” with 34% allowing investments in nuclear weaponry, according to Jefferies Financial Group Inc.’s fourth-annual ESG and defense survey.

Bitcoin struggled for a second straight week, remaining below the $80,000 threshold and reaching its lowest level in over five weeks. BTC is currently down approximately 13% year-to-date and sits ~39% below its October 2025 record high.

Global equity markets moved modestly higher this week as first-quarter earnings season continued to deliver strong results.

Despite the move lower late last week, U.S. Treasury yields are still holding well above recent lows and close to highs not seen in more than a year. By contrast, risk assets are firmly bid: U.S. equities have been routinely touching new historical highs, and credit spreads over Treasuries remain tight.

The White House’s decision to take a 9.9% stake in Intel Corp. is looking like very shrewd business indeed. Since the government bought in at $20.47 a share last August, the American chipmaker’s surging stock price has delivered the US a $43 billion return.

Gold has dropped more than 11 percent from its all-time high of just over $5,102 an ounce in January, and selling pressure continues to dominate the market. A well-established mainstream narrative is driving the bearish sentiment.

Despite these higher costs, a projected 45 million Americans are expected to travel at least 50 miles from home this weekend, setting a new record. Close to 40 million will drive while some 3.7 million will fly.

You don’t have to go very far to find lots of negative commentary in the popular press about the current state of the US economy. High gas prices (due to a “war of choice”) are squeezing consumers’ budgets, and so the economy is headed for a ditch.

Yes, we have been there before, only to be disappointed. But the market smells a real settlement to open Hormuz, and WTI oil briefly dipped below 90 for the first time in weeks. If an opening occurs, expect the market to continue its march upward, as the momentum trade gathers strength.

Despite headwinds from rising oil prices, fundamentals have remained strong. The S&P 500 has notched 18 record highs year to date and, more importantly, surpassed our prior target of 7,250. Following a standout 1Q earnings season, we are raising our 2026 earnings per share (EPS) estimate to $326 from $300.

This week marked the passing of former Massachusetts Congressman Barney Frank. His signature legislation, the Dodd-Frank Act of 2010, was the most recent increment in a long-running history of tighter financial regulation. Some of those rules are now coming under scrutiny, with the goal of making bank lending more competitive.

This piece examines the distinction between volatility and drawdown risk in portfolio construction, and why managing routine market fluctuations may not address the drivers of long-term wealth outcomes. The article is attached as a Word document, and the related chart is included as a separate image file.

The SpaceX initial public offering prospectus is more than 400 pages of rocket fuel-grade ambition. It is also an extended warning for investors in Tesla Inc. who aren’t named Elon Musk.

On May 26, 1896, Charles Dow calculated a simple arithmetic average of 12 industrial stocks and arrived at a closing value of 40.94. Now, exactly 130 years later, that same benchmark has crossed the historic 50,000 threshold.

Seven of the nine indexes on our world markets watch list posted year-to-date gains through May 26, 2026.

New AdvizorPro data shows RIAs broadened their ETF lineups in Q1 2026, leaning into real assets, active managers, and defense strategies.

The 2026 tax season is barely in the rearview mirror, but for advisors and their clients, this is when the real work begins. Right after filing, everything is still fresh. Clients remember what surprised them, what felt off, and where they may have missed opportunities. That awareness doesn’t last long.

Those driven to give to the point of harming themselves may be acting less from generosity than from deeply ingrained obligation, guilt, and fear. Helping clients navigate these conflicts requires compassion and a willingness to help them explore the emotional complexity of their money decisions.