Even if armchair investors are fleeing private credit or panicking that their unlisted shares in Anthropic PBC are now invalid, the long-term trend is clear: Public markets keep losing ground to private funds.

Sustainable investing in fixed income has come of age. Against a backdrop of heightened geopolitical tensions, persistent economic and trade uncertainty, sustainable fixed income continued to demonstrate its appeal in 2025.

Stocks’ rally off the March 30 lows has been nothing short of wild, with internal market dynamics showing some performance divergences that we haven’t seen for decades. For example, in the first 6 weeks of the rally, the S&P 500 Growth index beat the S&P 500 Low Volatility Index by more than any other 6-week window on record.

At first glance, the retreat of foreign asset managers is ominous. Signs of a domestic retail frenzy are everywhere. Cash deposits in local brokerage accounts have reached 137 trillion won ($91 billion), a two-third jump from six months ago.

Emerging markets (EM) are using low-cost renewables to cut fuel imports, stabilize power costs and improve energy security—positioning EM as the growth engine of the energy transition. Countries and companies that leverage their dominance in critical minerals and green technology could pull ahead, creating dispersion in potential outcomes for investors.

Model portfolios are a key pillar for asset managers competing for advisor and investor attention. They offer straightforward, pre-packaged tools that help investors target and achieve specific financial goals. Designing and operating models, however, takes a particular set of skills. Goldman Sachs Asset Management recently made a big hire therein.

With mega tech AI capital expenditure projected to cross a staggering $660 billion to $750 billion, according to estimates from firms like Goldman Sachs, CreditSights and Bloomberg, saying the stakes are high for Nvidia and the AI ecosystem is an understatement. It’s no wonder we can focus on little else this week.

While most institutional investors recognize that private equity and public equity share similar economic risks, they often seem to ignore how their aggregate equity portfolio is affected by their substantial allocation to private equity.

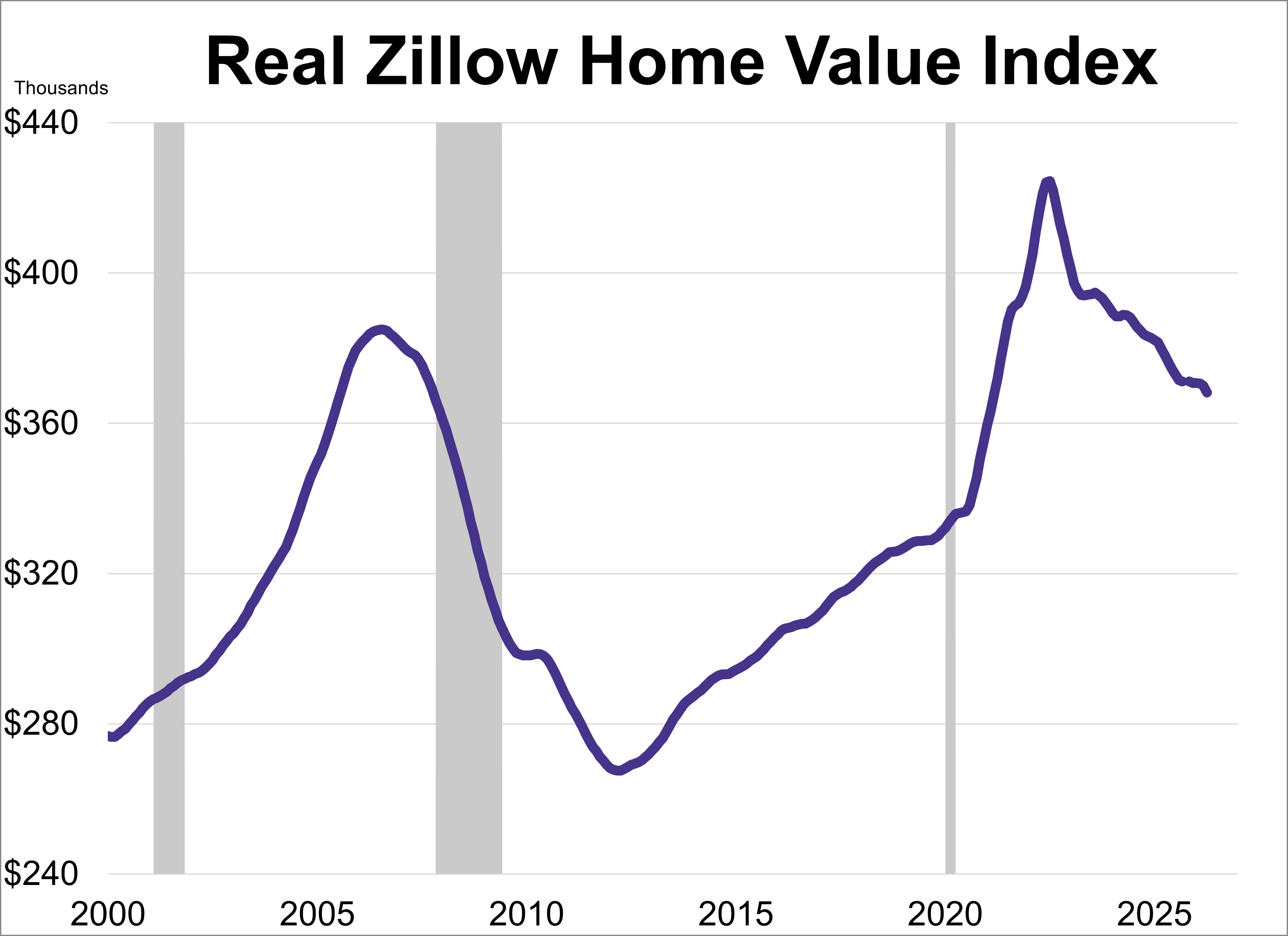

Home values continued their upward trend in April, according to the Zillow Home Value Index. However, after adjusting for inflation, real home values dropped sharply, remaining at their lowest level in over five years.

Join the experts at SS&C ALPS Advisors and VettaFi for a 30-minute discussion on May 21st at 12:30 pm ET on how the war has changed the playing field for North American midstream companies with impacts enduring well beyond the price spike.

The Kansas City Fed Manufacturing Survey revealed regional activity continued to increase in May. The composite index came in at 8 this month, down slightly from 10 in April but still indicating continued expansion.

At Google’s developer conference, which is being held near its Mountain View, California, headquarters this week, Chief Executive Officer Sundar Pichai started his keynote by emphasizing the remarkable reach of Google’s services. Thirteen have more than a billion users, he said, and five of them have more than 3 billion.

There’s a whiff of panic among investors these days. US Treasury yields have climbed to levels unseen in more than a year at the same time as a furious rally has left stocks near all-time highs. Surely, both moves can’t coexist for long, goes the narrative.

Wall Street is racing to turn computing power into a tradable commodity with the first ETFs being filed even before the futures contracts they would track have started to trade.

Nvidia Corp., facing more investor skepticism, used its latest quarterly report to tout progress in diversifying the company, which aims to rely less on the giant data center operators that have fueled its runaway growth.

Najimah Roberson, a lifelong renter, spent the past two years searching around Harrisburg, Pennsylvania, for a home she could afford — getting outbid nearly 30 times along the way.

In the past year, new models from industry leaders have continued to boost AI’s capabilities. According to various capabilities tests, Anthropic’s Mythos model has leapfrogged other AI models – including in the ability to thwart or support cyberattacks.

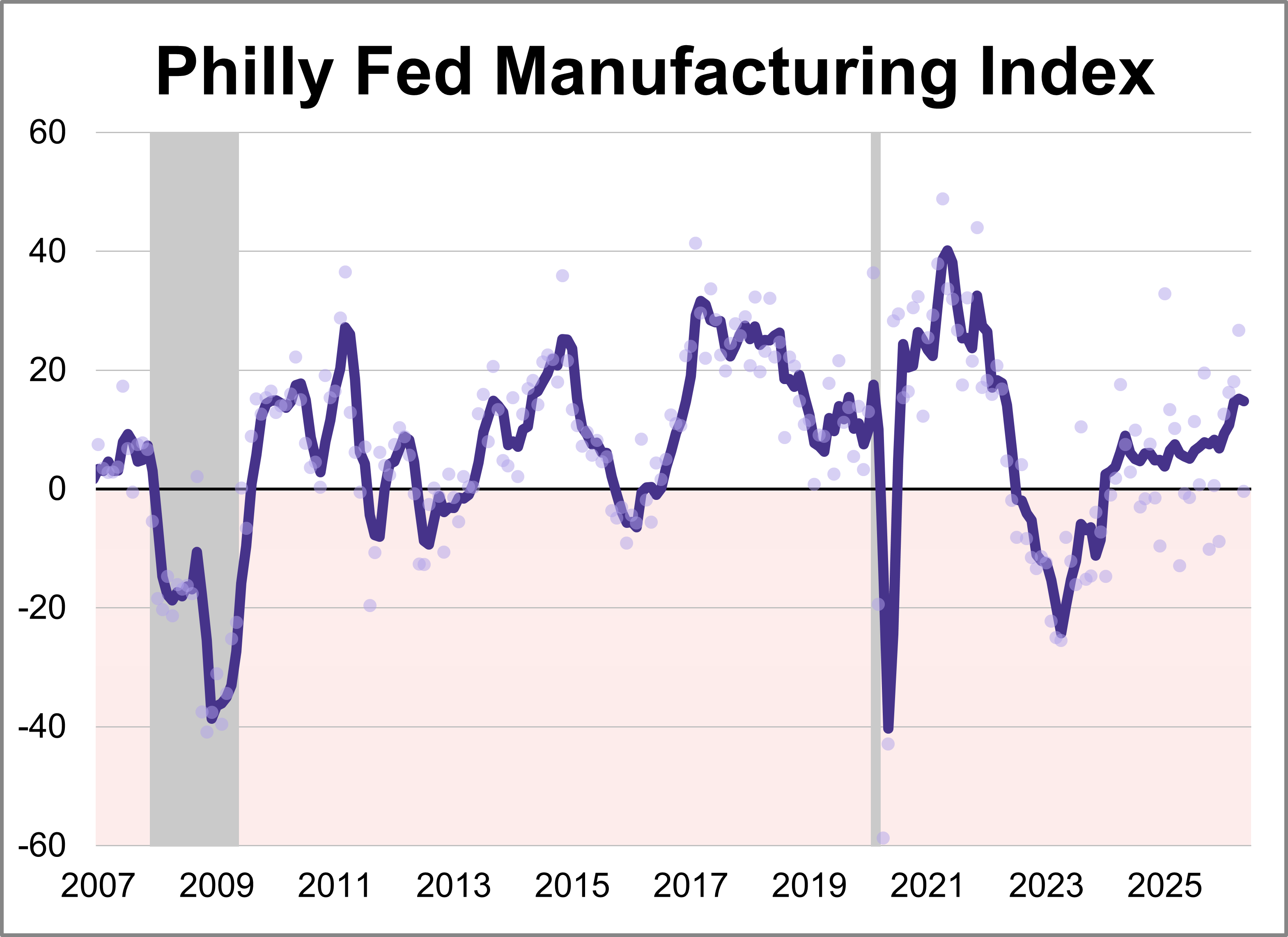

The latest Philadelphia Fed manufacturing index showed activity weakened in May, with the index sinking 27.1 points to -0.4. The latest reading marked the lowest level for the index this year and was worse than the forecast of 17.6.

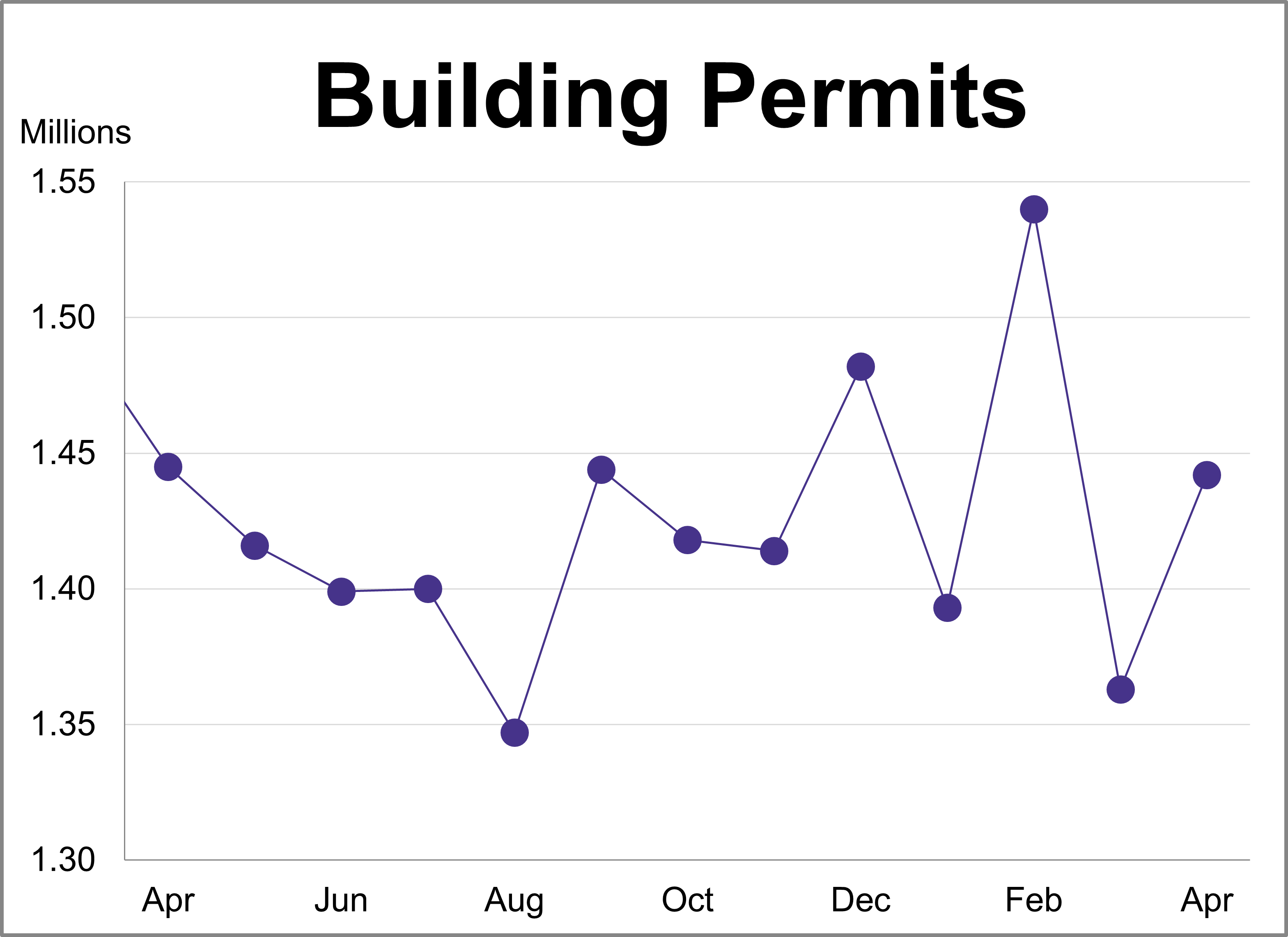

Building permits rose 5.8% to a seasonally adjusted annual rate of 1.442 million. The latest reading exceeded the forecast of 1.380 million.

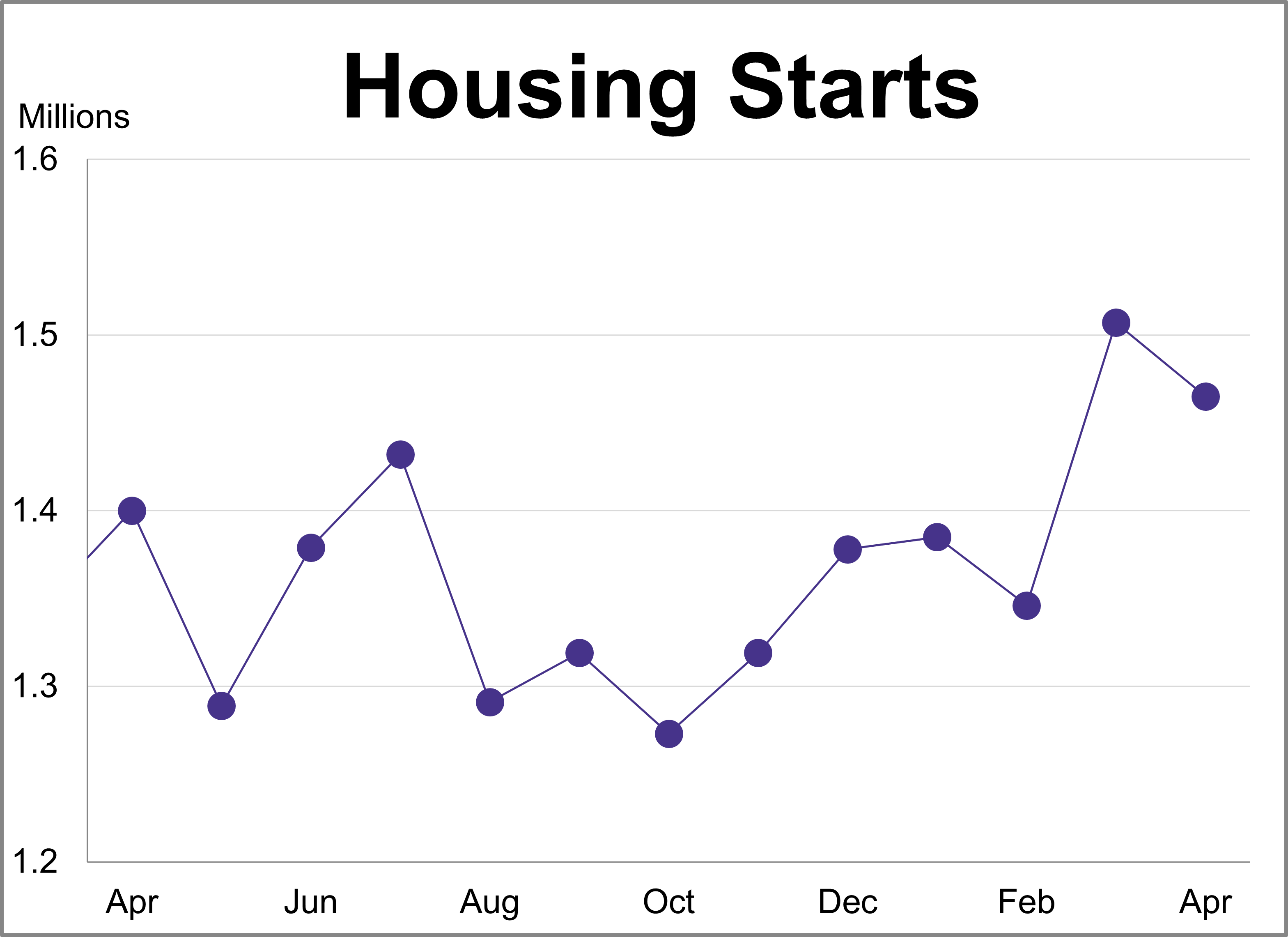

Housing starts fell 2.8% in April to a seasonally adjusted annual rate of 1.465 million. The latest reading exceeded the projected 1.420 million.

Right now, AAI’s two highest 10-year expected return forecasts are for large-cap value equity strategies outside the United States—Emerging Markets RAFI and Dev ex US Large RAFI. AAI’s expected return model anticipates valuations for equity strategies to mean revert and therefore tends to elevate out-of-favor regions and styles, predicting higher future returns for recently underperforming equity indices.

Enterprise software is undergoing its most significant reset in a generation. Artificial intelligence (AI) is reallocating value within software—creating clear winners and exposing vulnerabilities in business models that have worked well for the past two decades. We believe investors who treat software as a uniform asset class will make costly mistakes.

GMO has posted a new 7-Year asset class forecast as of April 30, 2026.

Institutional investors have spent years hearing about the promise of artificial intelligence. That phase is giving way to a more practical question: not whether AI can create more scale, but whether that scale can be governed, validated, and translated into better fiduciary decisions. For OCIO providers, AI without discipline is not an advantage.

In fixed income investing, trade execution plays an important role in overall portfolio performance. The ability to source bonds efficiently, invest capital thoughtfully and execute trades at competitive prices can directly affect investor returns.

The consumer is still spending, but with a higher level of caution. Inflation remains a persistent pressure point, particularly for lower- and middle-income households. This has caused the U.S. personal saving rate to fall to 3.6% as of March 2026, leaving significantly less breathing room for discretionary purchases.

LPL Research examines rising inflation risks amid geopolitical tensions, while resilient growth and strong investment support continued expansion.

It’s human nature to allow familiar patterns to guide our decision-making processes. But it’s just as important to recognize when changing conditions warrant a rethink. Return patterns in global equity markets appear to be shifting in ways that should prompt investors to revisit their allocations.

The exchange-traded fund marketplace continues to expand. Now with more than $20 trillion in assets under management ($14 trillion in the U.S., growing at an 18% five-year annualized clip), 2026’s volatility and emerging investment themes have taken the universe to new heights.

The "four horsemen" of the labor market are the unemployment rate, hiring rate, layoff rate, and vacancy rate. Analyzing them together may sharpen investors' read on the economy.

Inflation surged higher in April, with the Consumer Price Index (CPI) jumping 3.8 per cent from 3.3 per cent in March and the Producer Price Index (PPI) up six per cent from four per cent in March. The increase in the CPI owed much to energy and food prices.

Alex Evangeli has traded ETF products since 2007. He founded and led the fixed income trading business at Virtu Financial in Europe before relocating to New York to trade and lead the development of fixed income trading technology for the ETF block business.

Join the experts at State Street Investment Management and learn how the broader macro context is influencing sector leadership and what it may mean for portfolio positioning.

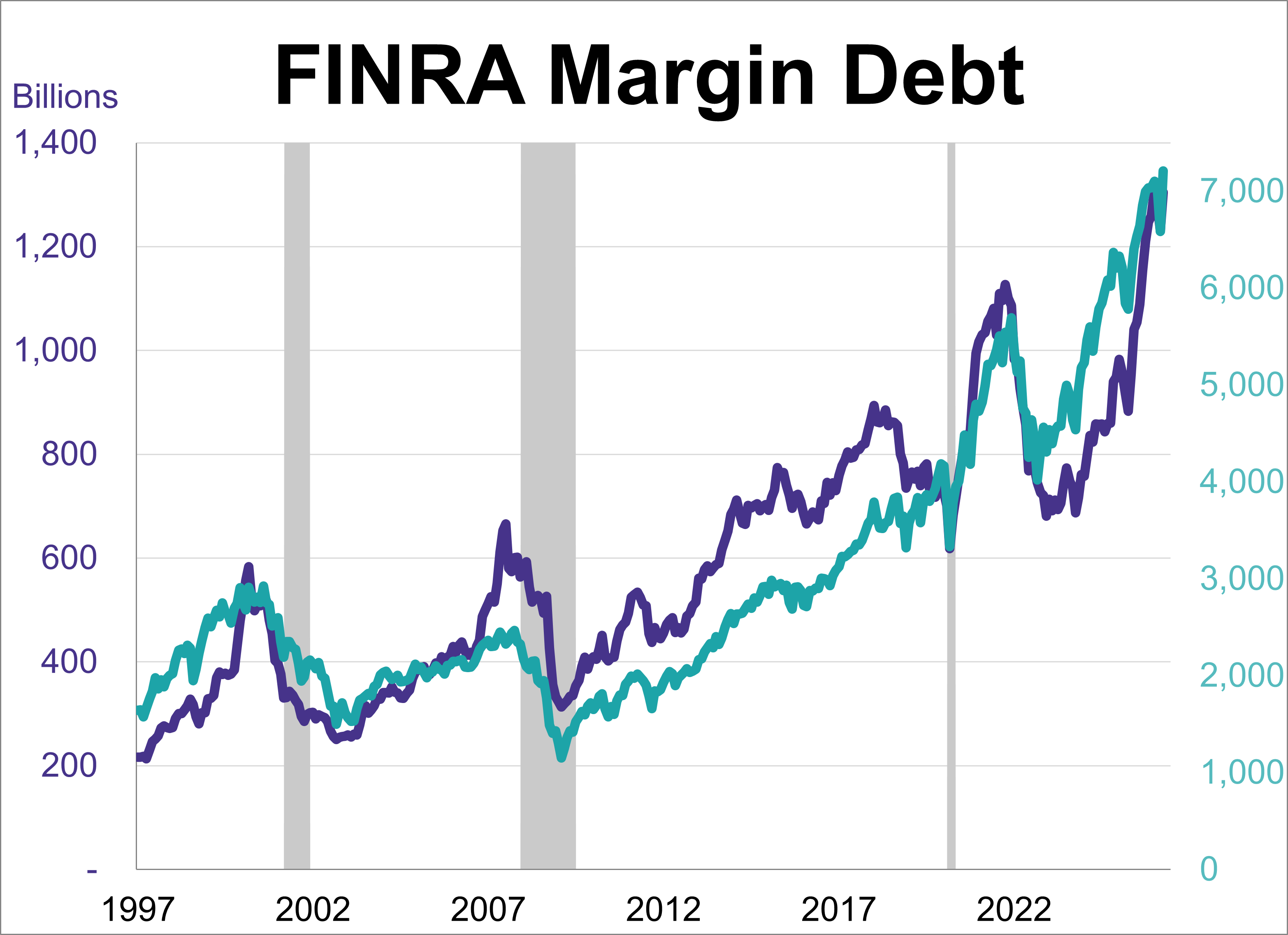

Margin debt rose for the first time in three months to a record high in April, coming in at $1.30 trillion. This marked a 6.8% increase from March and a 53.3% rise compared to the previous year.

The rapid deployment of artificial intelligence (AI) is evident; 99% of CEOs say their companies are investing in the technology. Apparently, AI is also quick at garnering assets. Launched less than three months ago, the Pictet AI Enhanced US Equity ETF (PQUS) is already approaching the $100 million mark in assets under management (AUM).

Reassessing legacy systems through a modern lens can help firms identify where closed, context-aware platforms may offer a stronger foundation for communication governance, operational efficiency and regulatory confidence. Open AI models helped kickstart automation in compliance. Closed platforms will likely make it sustainable.

The next generation may inherit substantial assets. Whether they inherit the health to enjoy them — or the burden of managing preventable family health crises — may matter just as much. Advisors who broaden the definition of legacy planning may be better positioned to protect both.

AI is unlikely to replace wealth managers — at least not in the foreseeable future. But it now has the power to expose the gaps between genuine, client-first investment advice and other approaches in a way the industry has not yet seen.

Space has evolved from a niche corner of the stock market into an area that offers the potential for diversity and growth. The euphoria around SpaceX’s market entry is driving fresh investor flows into the sector. Since the news of the offering first became public in early December, smaller space and related stocks have soared.

Turns out, loading up on technology giants isn’t the only route to better returns. Value companies, too, stand a decent chance of trouncing the market — as long as several conditions are met.

For much of the year, chip stocks have been powering the market higher. Now, Nvidia Corp.’s earnings have a chance to confirm that the rally has more room to run — or add another brick to investors’ wall of worry.

Although a lot has changed since our last quarterly, its central theme – dispersion – feels like it’s only become more pronounced. We wrote last time that ‘‘we believe we’re entering a new era of dispersion in the performance of financial assets.’’

Veteran strategist Jeff Currie said the world is in the early stages of a commodity supercycle that may last another decade or more as the artificial intelligence buildout collides with chronic underinvestment in energy and materials capacity.

On Friday, May 15, the 10-year Treasury yield closed at 4.59%, its highest level since February 2025. The 30-year Treasury yield closed near 5.12%, a level last seen in 2007. Those are significant moves because they reflect a repricing of the market’s inflation, growth, and Federal Reserve expectations.

The Texas Permanent School Fund bought more than 29 million shares totaling about $740 million worth of the State Street IG Public & Private Credit ETF, trading under the ticker PRIV, in the first quarter, according to a filing Friday.

Nineteenth-century oil processing plants used simple, column distillation of crude oil to produce kerosene, which was in high demand for lighting lamps. The process also yielded a dangerously flammable byproduct called gasoline which had no obvious use.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

That Buffett cash hoard has also created a lot of speculation, innuendo, and assumptions, which is what I want to walk through in today’s discussion. Primarily, what that cash hoard actually represents, the popular theories explaining it, and what it really costs shareholders to hold.

Markets ended last week under pressure as the optimism that had been building around a potential geopolitical breakthrough faded quickly. The China summit did not deliver the progress that had been hoped for. The Boeing aircraft order was smaller than expected; there was no meaningful movement on Iran; the Taiwan issue was brought forward in a way that unsettled markets; and the hoped-for easing of tensions around the Strait of Hormuz did not materialize.

One thing most people don’t know is that prior to the invention of the Fed, other than during wars, there was almost no inflation. Various sources including the Federal Reserve regional banks show the purchasing power of $1 in 1900 was the same as or higher than it was in 1800.